Social Security Seniors’ Benefits Cuts – What You Must Know

America’s piggy bank for retirees is running dry – what you need to know about Social Security payments for retirees

Many retirees rely heavily on Social Security, and potential benefit cuts could significantly impact monthly budgets.

Enhanced with ChatGPT

Written by Brett Holzhauer, Senior Financial Writer and graduate of the Walter Cronkite School of Journalism. Reviewed and edited by Deane Biermeier, Certified Financial Educator, at TrustedCompanyReviews.com.

It’s likely that at one point in your life, you’ve had more in bills than you have income. It’s an uneasy and stressful situation, and it’s the exact dilemma faced by the Social Security Trust Fund.

There’s no exact “doomsday” date when Social Security will be short of its needs, but current estimates from the Congressional Budget Office say it could be as soon as 2032. However, this doesn’t mean that Social Security is “going bankrupt.” But without Congressional action, retirees could see a 20-30% decrease in their monthly benefit payments.

The average Social Security benefit amount is currently $2,071. According to estimates, this recipient could lose roughly $400-600 each month.

Here’s everything you need to know about the current state of Social Security and how you can prepare financially for a potential loss in benefits.

How We Got In This Predicament

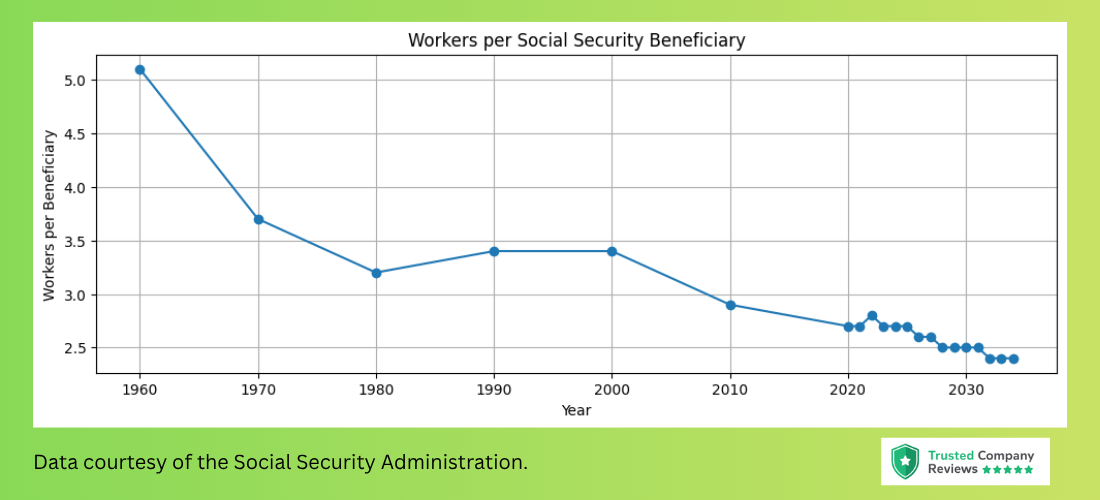

The financial calamity of Social Security comes down to one core issue: demographic changes.

In 1960, there were five workers for every Social Security claimant, meaning there was plenty of tax revenue flowing in to support post-career workers. Fast forward to today, and that ratio is estimated to be 2.6 workers for every retiree. The large baby boomer generation, mixed with a slowdown in birth rates, means that more money is being distributed than what is coming in, leading to the Administration having to use reserve funds to keep up with payments.

The future doesn’t look promising either, as the number of workers per retiree will decrease, according to the following data from the Social Security Administration.

The number of workers supporting each Social Security beneficiary has steadily declined, increasing pressure on the system.

Who This Impacts, and What It Means Going Forward

There are over 75 million people currently accepting Social Security benefits. The majority of recipients are over the age of 65 and receive only Social Security. There are others receiving benefits as well, including disabled workers, survivors of deceased workers, spouses of retired workers, and more. And according to AARP survey data, many of these recipients rely on these benefits. Nearly two in three retired Americans say they rely substantially on Social Security, while 21% say they rely on it somewhat.

However, this isn’t the first time Social Security solvency has come into question. This happened in the 1970s and 1980s, when the program nearly collapsed. But now with the sentiment of 2032 approaching, seven in 10 people (71%) are concerned that Social Security will not be available.

With workers paying hundreds of thousands, or even millions, over a lifetime into this social benefit, they are now calling on lawmakers to step in to make necessary adjustments. Here are some floated ideas for Congress to step in to keep this social program going.

Potential Solutions for Lawmakers

Raise payroll taxes:

In your paycheck, there is a line item for taxes. Part of that goes towards the larger Social Security Trust Fund. Workers and employers currently each contribute 6.2% of wages under the Federal Insurance Contributions Act. Even a small increase — such as raising the combined rate from 12.4% to around 13% or 14% — could extend the life of the program’s trust funds.

Lift (or eliminate) the payroll tax cap:

Social Security taxes only apply to wages up to $184,500 in 2026. Income above that level is not taxed for Social Security purposes. Removing or raising this cap would require higher-earning Americans to contribute more of their income to the system. Supporters argue it would generate significant new revenue, while critics say it would weaken the link between contributions and benefits.

Raise the retirement age:

When the system was created under the Social Security Act of 1935, Americans lived much shorter lives than they do today. Lawmakers could gradually increase the full retirement age beyond its current level of 67 for younger workers. This would reduce total lifetime benefits paid out and encourage people to stay in the workforce longer.

Adjust benefit amounts based on income:

Another option is to reduce benefits for higher-income retirees while preserving or even increasing payments for lower-income workers. This approach would shift Social Security slightly toward a need-based system rather than a strictly earnings-based benefit.

Change the cost-of-living adjustment (COLA):

Benefits currently increase each year based on inflation. Switching to a slower-growing inflation measure could reduce the rate at which benefits rise over time, lowering long-term costs.

What You Can Do To Prepare

It’s extremely unlikely that Social Security will cease to exist beyond 2032. However, relying on Social Security as a primary means of retirement may not be the best strategy.

Here are some ideas to consider to make Social Security a supplemental income in retirement, rather than relying on it as the primary source.

Begin saving for retirement on your own

You can begin saving for your own retirement today. Consider opening up an account like a Roth IRA, 401(k) through your employer, or a Health Savings Account (HSA).

Each of these can enable you to put money away for your post-working years, and give you more control over your financial future.

Pay down (or refinance) debt

It’s almost always a great idea to knock down any line items on your balance sheet. If you’re struggling with debt, consider looking at refinancing existing debt to minimize the interest you’re paying, or borrowing money using a personal loan or home to begin knocking down those balances. This could include medical debt, car debt, or credit card debt.

Diversify Your Retirement Income

Relying on a single income source in retirement can create unnecessary financial risk. Instead, aim to build multiple streams of income that work together.

This may include retirement accounts like IRAs or 401(k)s, taxable brokerage investments, rental income, part-time work, or other passive income sources. Diversifying your retirement income can help ensure that if one source falls short, you have others to supplement your monthly necessities.

Further Reading:

- 401(k) Hardship Withdrawals Rise as More Workers Tap Retirement Savings

- Saver’s Credit Explained: How It Works and What’s Changing