Saver’s Credit Explained: How It Works and What’s Changing in 2027

Key changes to the Saver’s Credit explained simply

The savers credit can help lower your tax bill and support retirement savings

Image courtesy of iStock

You’ve likely heard of employers matching a portion of your 401(k) contributions. For those who qualify, the government is now giving you a direct match starting in 2027.

This has been known as the Saver’s Credit, which has been a tax credit. Starting next year, this is now a match deposited directly to your retirement account–no tax forms needed. This “free money” can be a substantial start to your investing journey.

Here’s what you need to know about the changes, and how you can double-dip before the end of the year.

What is the Saver’s Credit?

The Saver’s Credit is a federal tax credit designed to reward low- and moderate-income workers for putting money into retirement accounts. If you contribute to an eligible retirement account and meet the income and eligibility rules, the credit can reduce the amount of federal income tax you owe.

This matters because a tax credit is more valuable than a tax deduction. A deduction lowers your taxable income, but a credit lowers your tax bill dollar for dollar. So if you qualify for a $1,000 Saver’s Credit, that can shave $1,000 off what you owe in federal income taxes. The catch is that the Saver’s Credit is nonrefundable, which means it can reduce your tax bill to zero, but it will not create a refund beyond that. That limitation is a big reason the credit has never been as powerful in practice as it looks on paper.

A simple way to think about it: if someone contributes $2,000 to an IRA and qualifies for the 50% rate, they could claim a $1,000 credit. That is a meaningful incentive to get started, especially when a significant number of people have no retirement savings at all.

The problem is that many eligible workers either don’t know the credit exists or don’t owe enough tax to fully benefit from it. That gap is a big reason Congress is replacing the Saver’s Credit with the new Saver’s Match starting with 2027 tax returns filed in 2028.

Related Articles:

- 8 Ways To Legally Reduce Your Income Tax

- Federal Student Loan Debt Changes – Here’s What You Need To Know

Who Qualifies for the Saver’s Credit

You may qualify for the Saver’s Credit if you meet these criteria:

- Must be at least 18 years old

- Cannot be a full-time student

- Cannot be claimed as a dependent on someone else’s tax return

- Must have adjusted gross income (AGI) below IRS limits

2026 income limits:

- $80,500 for married couples filing jointly

- $60,375 for heads of household

- $40,250 for single, married filing separately, or qualifying surviving spouse filers

The IRS provides a calculator where you can input your financial numbers to see if you qualify for the Saver’s Credit. You can find the numbers you need on your most recent tax return.

What’s Changing in 2027: The Saver’s Match

The shift to the Saver’s Match comes from the SECURE 2.0 Act, which was signed back in 2022.

One key problem lawmakers aimed to fix: the Saver’s Credit hasn’t worked as well as intended. Because it’s a nonrefundable tax credit, many eligible savers don’t receive the full benefit if they owe little or nothing in taxes. That means the people who need the most help building retirement savings often get the least value.

Starting in 2027, the Saver’s Match replaces that structure entirely. Here’s how it works:

- The federal government will match 50% of your eligible retirement contributions

- The maximum match is $1,000 per person (or $2,000 for married couples)

- The match is deposited directly into your retirement account, not issued as a tax credit

- Eligible accounts include IRAs and employer-sponsored plans like 401(k)s

This change makes the benefit more immediate and easier to understand. Instead of waiting until tax season to see a potential reduction in what you owe, you’ll see the government’s contribution show up alongside your own savings.

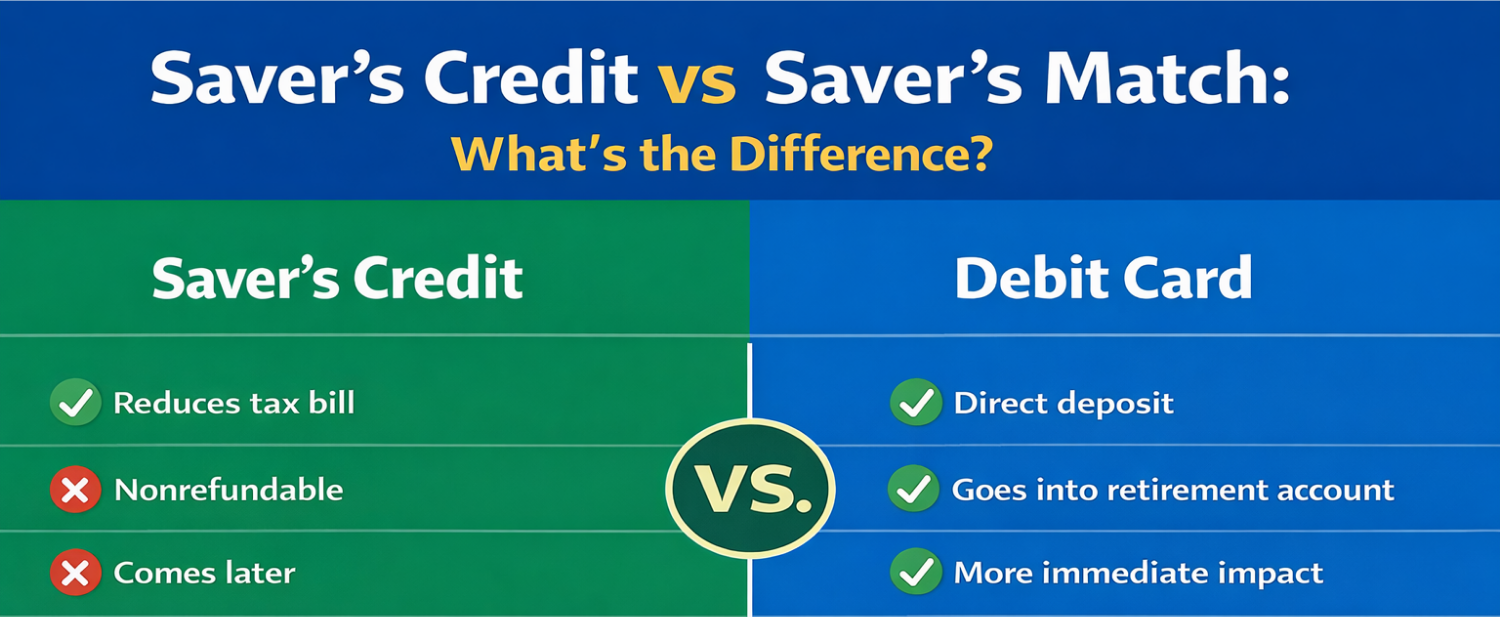

Saver’s Credit vs Saver’s Match: What’s Changing?

A side-by-side look at what the savers credit is and how it compares to the new saver’s match starting in 2027

A Realistic Example

Let’s say you’re a single worker earning $35,000 per year and contributing $2,000 annually to a Roth IRA. Here’s how the Saver’s Credit can positively impact your retirement savings results:

| Scenario |

Your Annual Contribution |

Government Match | Total Annual Investment |

20-Year Value (7% Return) |

| Without Saver’s Match |

$2,000 |

$0 | $2,000 |

~$82,000 |

| With Saver’s Match |

$2,000 |

$1,000 | $3,000 |

~$123,000 |

| Difference |

— |

— | +$1,000/year |

+$41,000 |

Related Article: How to Spend Your Tax Refund Smartly

How You Can Double Dip, Today

There’s a short window where you can take advantage of both the Saver’s Credit and Saver’s Match.

If you qualify now, start by using the Saver’s Credit while it still exists. Contributions you make in 2026 can reduce your tax bill when you file, giving you an immediate benefit for saving. Then, starting in 2027, shift your focus to maximizing the Saver’s Match. This means contributing at least enough to unlock the full government match.

Here’s the simple playbook:

- 2026: Contribute to a retirement account and claim the Saver’s Credit

- 2027: Contribute again and receive up to a $1,000 direct government match

- Ongoing: Keep contributing consistently to build long-term growth

Even if you’re only able to contribute a few thousand dollars per year, these back-to-back incentives can create real momentum. You get a tax break first, then direct government contributions the following year. Both help accelerate your retirement savings.

Where To Get Started Today

Start by opening or using an existing retirement account. This could be an IRA through a provider like Vanguard, Fidelity, or Charles Schwab, or a workplace plan like a 401(k). Then focus on contributing what you can. Even a few hundred dollars gets you in the game, and contributing up to $2,000 positions you to take full advantage of future matching benefits.

Here’s a simple checklist to ensure you get the government incentives you qualify for:

- Open or log into an IRA or employer-sponsored retirement plan like a 401(k)

- Contribute what you can for the current tax year

- Check your income to confirm you qualify for the Saver’s Credit

- Set up automatic contributions so you stay consistent

- Plan ahead to contribute at least $2,000 in 2027 to unlock the full match

Small, consistent contributions combined with government incentives can build into something meaningful over time.

Bottom Line

Saving for retirement is an essential part of your financial life. It’s never too early to start planning, and the longer you wait, the more you potentially miss out on compound interest and gains in the stock market.

By investing today and taking advantage of both the Saver’s Credit today and the Saver’s Match next year, you can start building your nest egg for your post-working years.

Related Article: Millions of Car Owners Face Late Car Payment Difficulties