How to Spend Your Tax Refund Smartly

Smart ways to spend your tax refund and plan ahead financially.

Explore how to spend your tax refund across savings, debt payoff, and financial goals.

iStock Images

Taxpayers are seeing larger-than-normal refunds this tax season, with the average tax refund at $3,462 – 11% higher than last year. This is a significant financial boost for millions of taxpayers, especially those who don’t have $1,000 set aside for an emergency. This has many asking how they should spend their tax refund, with many choosing to put it toward necessities or paying down debt.

We put together a checklist of ways you can use your tax refund this year to propel your financial picture forward, depending on your current financial picture.

Brett Holzhauer is a senior financial writer and editor with over a decade of experience covering personal finance, investing, and the U.S. economy. His work has been featured in Forbes and CNBC, where he focuses on helping readers make sense of real-world financial challenges.

Key Takeaways

|

Related Article: What to Do With Extra Money

Why Your Tax Refund Matters More Than You Think

For many households, their tax refund is one of the largest lump sums of cash they’ll see all year. And because it arrives all at once, it often feels different from a regular paycheck.

Psychologically, a tax refund can feel like a bonus or “extra” money, even though it isn’t. A tax refund is exactly that – a refund. You overpaid your taxes throughout the year and are simply getting that money back. But because it doesn’t show up in your monthly budget, it’s easier to spend it quickly or without a plan.

A better way to think about your refund is to see it as delayed income. Instead of treating it like found money, treat it like a financial reset button.

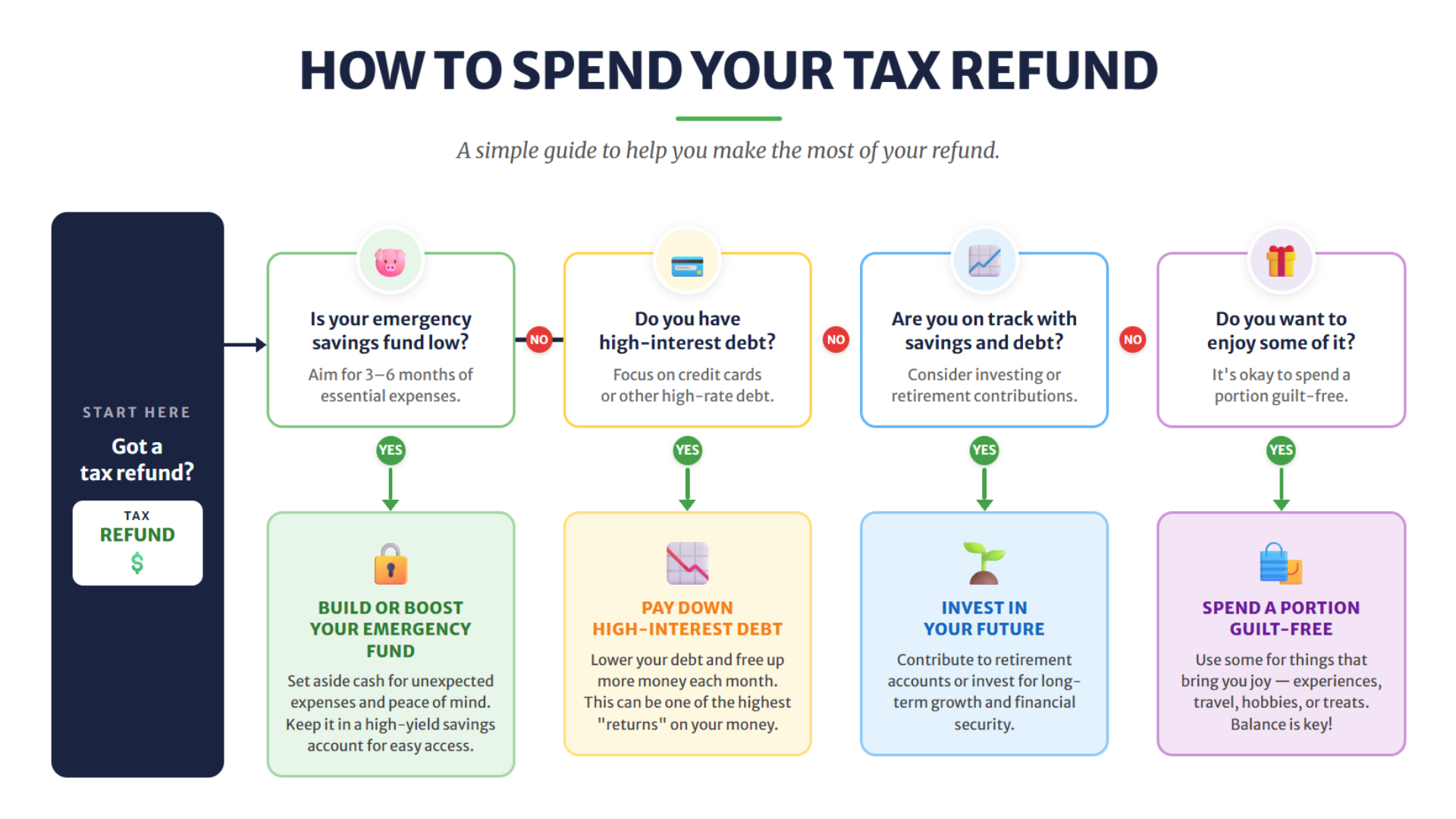

So if you’ve received a solid tax refund this season, the following checklist outlines common approaches taxpayers take when deciding how to allocate a refund.

A simple flowchart outlining common ways to decide how to spend your tax refund.

Step 1: Cover Your Financial Basics First

Before you invest or spend your tax refund, make sure your foundation is solid. For many households, shoring up financial fundamentals is a common first priority before directing funds toward growth-oriented strategies.

Build or Boost Your Emergency Fund

Start by setting aside cash for unexpected expenses. A good target is three to six months of essential expenses. That might sound high, but even getting to one month is a meaningful step in the right direction.

Keep this money in a safe, accessible place. A high-yield savings account or short-term Treasury fund can earn interest while still giving you quick access when you need it. The goal here is stability and peace of mind.

Pay Down High-Interest Debt

For those carrying high-interest credit card balances, directing refund dollars toward that debt is a strategy many financial planners highlight. Historically, eliminating a 20% interest rate obligation has the mathematical effect of a comparable return

| Debt consolidation is one option some borrowers explore when managing multiple high-interest balances. It’s worth researching to understand whether it fits a given financial situation. |

Step 2: Use Your Tax Refund to Get Ahead

Once your monthly budgeting basics are covered, your tax refund can shift from protection to growth. This is where you start building long-term wealth.

Invest for Long-Term Growth

Putting even a portion of your refund into the market can pay off over time. Options like a Roth IRA or a standard brokerage account give you exposure to long-term growth through stocks and index funds.

The real advantage is compounding. As a hypothetical illustration: $3,000 growing at a historical average rate of 7% annually could reach more than $11,000 over 20 years — though actual market returns vary and are not guaranteed.

Contribute to Retirement Accounts

Retirement accounts offer some of the best tax advantages available. For 2026, you can contribute up to $7,500 to an IRA (or $8,500 if you’re age 50 or older).

If you have freelance or side hustle income, a Solo 401(k) opens the door to much higher contribution limits. You can contribute as both the employee and the employer, potentially putting away tens of thousands of dollars, depending on your income.

Using your tax refund to kickstart or top off these accounts can meaningfully accelerate your long-term financial trajectory.

Step 3: Spend a Portion Guilt-Free

Not every dollar of your tax refund needs to be optimized. In fact, giving yourself permission to enjoy a portion of it can make your overall plan more sustainable.

The 80/20 or 70/30 Rule

A simple way to approach this is to split your refund. Put 70-80% toward financial goals like saving for a home or car, investing, or paying down debt. Then use the remaining 20-30% for something you actually want. This structure lets you make real progress while still feeling rewarded.

Smart “Wants” That Add Value

If you’re going to spend, spend with intention. Experiences like travel, time with friends, or something you’ve been putting off tend to deliver more lasting value than impulse purchases.

How to Adjust Your Withholding for Next Year

If you consistently receive a large tax refund, it may be worth adjusting your withholding. While it can feel like a bonus, a large refund usually means you’ve been overpaying taxes throughout the year.

The goal is to get closer to breaking even. That way, you keep more of your money in each paycheck instead of waiting for a lump sum at tax time. For many people, that extra cash flow can be more useful throughout the year, rather than waiting until tax season.

You can make this adjustment by updating your W-4 form with your employer. The IRS redesigned the form to be more straightforward, focusing on income, dependents, and any additional withholding you want to include. You don’t have to get it perfect, as even small tweaks can reduce the size of your refund and increase your take-home pay.

Final Thoughts

It’s normal to ask yourself how to spend your tax return. It can be tempting to treat this windfall as “free money,” but it’s actually money you’ve worked hard for. The government is simply giving it back to you after overpaying on your taxes for the previous year.

For many taxpayers, a refund represents one of the larger single cash events of the year — an opportunity some use to address savings gaps, reduce debt, or begin building an investment position.

Related News: 7 Smart Money Moves to Make Before the End of 2026 – A Financial Checklist