Your credit card habits can reveal a lot more than just your spending. They can reflect how you think about money, risk, and the future.

Getting a credit card seems simple. You use it, maybe pay it off, and sometimes earn rewards along the way. But if you look a little closer, it’s not just the about card you carry. It’s how you use it that tells the real story.

Key Takeaways

|

Your credit behavior offers insight into how you manage your money. The key is understanding what those habits mean, and whether they’re actually helping you move forward.

From reward maximizers to cautious users, what you do with your credit cards is far more important than which ones you actually have. This guide reveals some of the hidden meanings behind that thought.

What Your Credit Card Habits Reveal

If You Focus on Rewards and Points

If you’re constantly thinking about points, miles, or cashback rewards, you’re likely someone who wants to maximize every dollar you spend. You’re intentional, strategic, and probably enjoy getting something extra out of everyday purchases. This sentiment can extend into other financial approaches, such as investing strategies.

This approach works well, especially if you’re paying your balance in full each month. Travel rewards cards, in particular, appeal to people who value flexibility and experiences. Cards like the Chase Sapphire Preferred® Credit Card are designed for this type of user, offering strong rewards and redemption options.

Where it can go wrong is when rewards become the reason for spending. If you’re chasing points but carrying a balance, the interest charges can quickly outweigh any benefits.

Your credit card habits—like paying in full or carrying a balance—can reveal how you approach money and financial decisions.

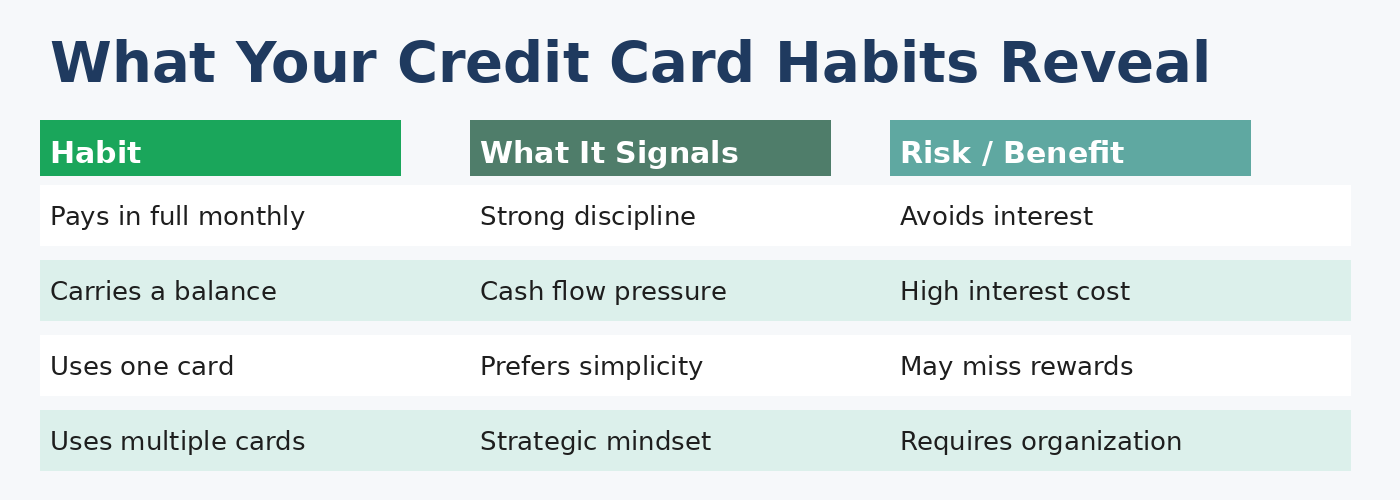

If You Carry a Balance Month to Month

If you regularly carry a balance, it may signal that you’re relying on credit to manage cash flow, or that regular living expenses are stretching your budget beyond what it can handle.

This isn’t uncommon, but it does come at a cost. Interest rates on credit cards are typically high, and paying interest on them can make even small purchases much more expensive.

For some, this strategy is temporary and intentional. For others, it can become a cycle that’s hard to break. If this sounds familiar, shifting toward paying down balances and reducing reliance on credit can make a significant difference.

Debt consolidation is a possibility at this point, but it’s crucial to understand that consolidating debt and not changing habits or spending can cause more trouble down the road.

If You Always Pay Your Balance in Full

Paying your balance each month, or multiple times each month, is a strong financial habit that also suggests that you likely have strong financial discipline and a clear understanding of how to avoid interest charges and use credit in general.

People in this category often:

- Stay organized with due dates

- Avoid unnecessary debt

- Use credit as a convenience, not a necessity

This is one of the strongest indicators of healthy credit use and is one of the most effective ways to build your credit score over time.

Related Article: Can I Use My Credit Card as Debit? What to Know Before You Try

If You Use One Card for Everything

If you prefer using a single card for all purchases, you likely value simplicity and consistency. You don’t want to juggle multiple accounts or track rotating reward categories. You just want something that works.

This is where flat-rate cashback cards can be beneficial. Options like the Wells Fargo Active Cash® Credit Card offer straightforward rewards on every purchase, making them ideal for everyday use. There are several other options listed in our overview of the best catch-all credit cards.

This habit reflects efficiency, as you’re not trying to optimize every detail; you’re more focused on keeping things manageable.

If You Open Cards for Specific Goals

Some people use different credit cards for different purposes. Card users in this category often focus on travel, business expenses, or specific reward categories. This approach suggests a more advanced understanding of how credit works.

Business owners, for example, often use separate cards to track expenses and manage cash flow. Cards like the Chase Ink Business Unlimited® Credit Card can be handy for this type of use.

While this habit reflects strategy, it also requires organization. Without careful tracking, multiple accounts can become difficult to manage.

However, strong habits, such as paying the balance each month and avoiding maxing out business cards, are still critical in this scenario.

If You Keep Credit Simple or Minimal

If you avoid multiple cards or don’t pay much attention to rewards, you may prefer a more straightforward approach to money. You likely value control over complexity.

There’s nothing wrong with this mindset. In many cases, it leads to fewer mistakes and a clearer understanding of your finances.

However, it can also mean missing out on potential benefits if you’re not taking advantage of rewards or credit-building opportunities.

What Your Credit Card Doesn’t Say About You

While your habits can reveal patterns, they don’t tell the full story.

Your credit card doesn’t define:

- Your overall financial health

- Your income or net worth

- Your long-term financial success

Two people can have the same credit card and use it in completely different ways. One may pay off their balance each month, while the other carries debt and pays interest.

How you use credit in general is a much more effective way to measure your overall financial well-being.

The card itself isn’t the determining factor—your behavior is.

Should You Choose a Credit Card Based on Personality?

It’s tempting to choose a credit card based on identity. thinking of yourself as a traveler or a rewards maximizer, and choosing a card solely for those purposes. But in reality, personality isn’t the most important factor.

A better approach is to choose a card based on how you actually use credit.

For example:

- If you carry a balance, a lower interest rate will likely matter far more than rewards

- If you pay in full, rewards and perks become more valuable

- If you’re building credit, simplicity and reliability are key

The right card isn’t about who you think you are. Rather, it’s about what works best for your financial habits. An action step toward better financial management is knowing when you should and shouldn’t use a credit card.

Here’s the thing: “Your credit matters because it affects your ability to get a loan, a job, housing, insurance, and more. If you understand what your credit is, it’ll help you protect it.” That’s right from the Federal Trade Commission’s Consumer Advice Page.

Pro TipFrom our on-staff Certified Financial Educator Okay, true confession time. I really did this. Yes, even as a financial professional. It’s a good indicator that marketing is powerful, especially when it comes to financial products. Years ago, I fell for one of those “50,000 bonus miles” offers and signed up for an airline credit card tied to a carrier I barely used. I liked the idea of being a “traveler.” It felt like the right move, but it was a purely emotional decision. The problem? I already had an airline miles card that I used all the time. This new one didn’t fit how I actually traveled. The routes were limited, and I already had a card I liked (and still use). I used the bonus miles from the new card. But then it just sat there in my wallet until I finally got sick of paying the annual fee for something I wasn’t using. The lesson? And if you’ve done something similar, you’re not alone. Even people who understand credit well sometimes have to learn some lessons the hard way. |

What Matters More Than the Type of Card You Have

No matter which credit card you use, your habits will always matter more than the features.

Here are the fundamentals that make the biggest difference:

- Making payments on time: This is the single most important factor regarding your credit score.

- Keeping your balance low: Maintaining a low credit utilization ratio can help improve and maintain your score.

- Avoiding unnecessary interest charges: Paying your balance each month saves money,

- Managing your credit limit responsibly: Don’t rely on your full available credit. Use only a small percentage of the credit available to you.

These behaviors are what truly determine whether your credit cards will work for you or against you.

When Credit Works for You (And When It Doesn’t)

Credit cards work best when they support your financial goals. They can help you build your credit score, manage large purchases, and create flexibility in your budget when used correctly.

But they stop working when they become a substitute for income or a way to sustain spending you can’t afford.

If you’re using credit intentionally and managing it well, it can be a powerful tool. If not, it can quickly become a source of long-term debt.