8 Ways To Legally Reduce Your Income Tax

Reduce income tax through credits, HSAs, retirement plans, and charitable giving.

Tax planning strategies that may help reduce income tax over time.

iStock Images

You may have just completed your taxes for 2025 and been surprised at a larger-than-normal tax refund. So far this tax season, filers are receiving an average refund of just over $3,500, according to the IRS – an 11% increase from the year prior. Despite higher refunds, taxes remain one of the largest bills you will pay throughout your lifetime.

The average American will pay $524,625 in taxes throughout their lifetime — roughly one-third of estimated lifetime earnings, according to a recent study. While a refund this year can be a great way to improve your financial picture, there may be additional strategies to consider in 2026 that could help reduce the income tax you owe.

Here are several strategies to consider this year, along with the context for why this is important to your own financial journey.

Key Takeaways

|

Related Article: What to Do With Extra Money

Income Tax Is Big Money

Income taxes are a vital source of revenue for the U.S. government for a simple reason: they scale with the economy and are easy to collect. As wages rise and employment grows, tax revenue increases simultaneously, without Congress needing to overhaul the system. The widespread use of automatic withholding means the government gets paid in real time, rather than having to chase payments afterward.

In fiscal year 2025, the largest source of federal revenue was individual income taxes (50.7% of total revenue) – a whopping $2.66 trillion. In 2024, the average amount paid per worker in total federal and state income taxes was $12,582. This represents a significant portion of income, which is why many taxpayers look for ways to manage their tax liability more effectively.

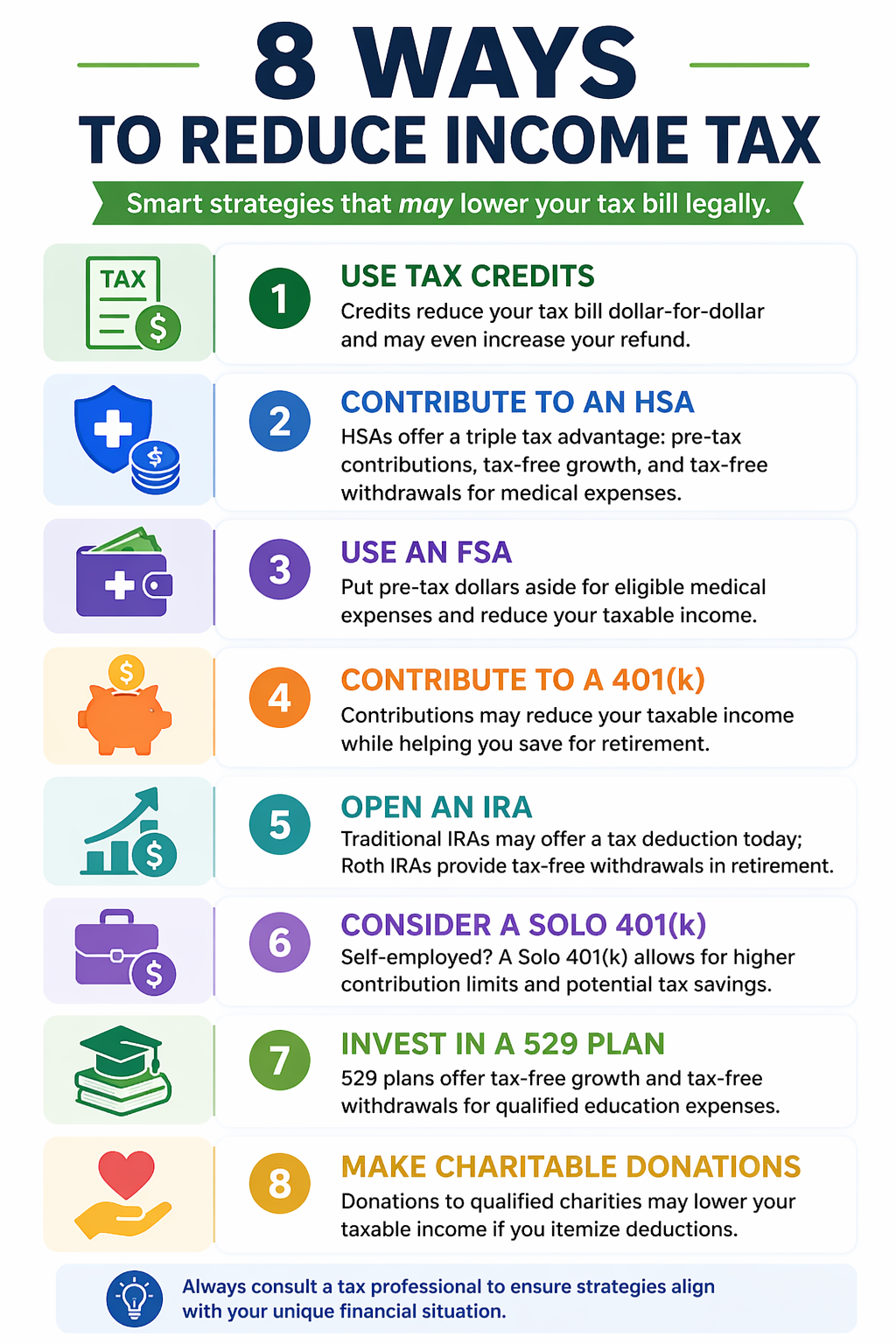

A visual breakdown of eight common strategies that may help reduce income tax.

Here are several ideas to consider to potentially reduce your income tax.

1. Review What Tax Credits You’re Eligible For

If you want to lower your lifetime tax bill, tax credits are one of the most powerful tools available. Unlike deductions, credits reduce your tax bill dollar-for-dollar. In some cases, they can even trigger a refund.

Here are some of the most widely used credits:

- Earned Income Tax Credit (EITC)

Designed for low- to moderate-income workers, the Earned Income Tax Credit can significantly reduce your tax bill. Eligibility depends on income, filing status, and number of children. - Child Tax Credit (CTC)

The Child Tax Credit provides up to $2,000 per qualifying child, with a portion potentially refundable. It’s one of the most common ways families reduce their annual tax burden. - Child and Dependent Care Credit

If you pay for childcare so you can work or look for work, the Child and Dependent Care Credit can help offset a percentage of those costs. - American Opportunity Tax Credit (AOTC)

The American Opportunity Tax Credit helps cover the cost of higher education, offering up to $2,500 per eligible student for tuition, fees, and course materials.

Pro tipYou may also explore tax software options to help organize and file future returns. |

2. Contribute to a Health Savings Account (HSA)

A Health Savings Account (HSA) is an account where you can put money away for future medical expenses and even invest it to grow the balance over time.

To have an HSA, you must have a high deductible health plan (HDHP). This is a type of medical coverage with higher minimum deductibles, typically designed for people who don’t see a doctor often. Here are the minimum deductibles for 2026, for both single and family coverage.

|

Coverage Type |

Minimum Deductible (2026) |

Max Out-of-Pocket (2026) |

|

Self-Only |

$1,700 | $8,500 |

| Family | $3,400 |

$17,000 |

This account is known for its triple tax advantage: money goes in pre-tax, can be invested and grow tax-free, and those funds can be withdrawn tax-free for qualified medical expenses. This structure allows some taxpayers to use HSAs both for current medical expenses and as part of longer-term financial planning.

For 2026, you can invest the following amounts:

- Individual (self-only): $4,400

- Family coverage: $8,750

- Age 55+ catch-up: +$1,000

3. Flexible Spending Accounts (FSAs) Work Too

A Flexible Spending Account (FSA) is similar to a Health Savings Account, where you can put money away on a pre-tax basis for medical expenses. For 2026, you can put away $3,400 in pre-tax funds.

The core difference with an FSA is that it’s employer-backed, and the funds are “use it or lose it.” They can’t be invested in the stock market and must be used within the year.

4. Contribute to Retirement Plans

There are several options to put money away for retirement, depending on your employment situation. Many workers have options like a 401(k) through their employer, which is a great way to reduce income tax and save for retirement simultaneously.

On top of your employer-sponsored plan, there are additional ways that you can take action today.

5. Open an IRA Too

On top of your employer-sponsored plan, you can also open an IRA (individual retirement account). While there are multiple types of IRA accounts, the two most widely known are the Traditional and Roth IRA.

The Traditional IRA can help you reduce your income tax, as the dollars you put in will give you a tax deduction at the end of the year. This means that your dollars can grow, and you will pay taxes on them when you withdraw the funds in retirement. Whereas a Roth IRA uses post-tax dollars, but the funds can be withdrawn tax-free after you turn 59.5 years old.

For 2026, IRA contribution limits are:

- $7,500 per year if you’re under age 50

- $8,500 per year if you’re 50+ (includes $1,000 catch-up)

6. If You Have A Side Hustle, Open a Solo 401(k)

If you earn any self-employment income, even a few thousand dollars a year, you can open a Solo 401(k) and allow for higher contribution limits compared to some other retirement accounts. You can contribute both as the employee, up to the standard 401(k) deferral limit, and as the employer, typically up to about 20% of net self-employment income.

To qualify, you must have self-employment income and no full-time employees other than a spouse. This includes freelancers, consultants, side hustlers, and small business owners. If you make money outside a traditional W-2 job, even part-time, you’re generally eligible to open and contribute to one.

It’s one of the most powerful tax moves available to freelancers. Contributions can reduce your taxable income today, grow tax-deferred or tax-free with a Roth option, and give you flexibility to scale contributions up or down based on your income each year.

Here’s how much you can contribute:

- Total max (employee + employer combined): $72,000 if you’re under 50

- If you’re 50+: Up to $80,000 (includes $8,000 catch-up)

- If you’re 60–63: Up to ~$83,250 with the higher “super catch-up”

Related Article: Notice CP30: IRS Underpayment Penalty Explained

7. Help Your Kids Save For Their Future

529 Plans: Simple, Proven Tax Benefits

A 529 plan gives you a few key advantages:

- Tax-free growth: Your investments grow without yearly taxes

- Tax-free withdrawals: Use the money for qualified education expenses, and you pay no federal taxes

- State tax breaks: Many states offer a deduction or credit for contributions

- Flexible use: Funds can cover tuition, housing, books, and more

You can even open one for yourself and change the beneficiary later.

Under IRS rules, unused 529 funds can also be rolled into a Roth IRA (with limits), which adds a layer of flexibility.

Trump Accounts: Still More Concept Than Strategy

Trump accounts are newly proposed government-funded investment accounts for kids. The idea is simple:

- Seed money at birth

- Families can contribute over time

- Investments grow tax-advantaged

Over 5 million children have already been given accounts, and the Wall Street Journal has summarized the account potential quickly: The Hack That Turns Trump Accounts Into Multimillion-Dollar Tax-Free Nest Eggs.

8. The Value of Donations

Charitable donations are a straightforward way to lower your tax bill.

You can now deduct up to $1,000 (single) or $2,000 (married) in cash donations even if you take the standard deduction, as long as you give to qualified nonprofits. If you itemize, there’s a new limitation: only donations that exceed 0.5% of your adjusted gross income (AGI) are deductible. That means smaller donations may not count unless you give enough to clear that threshold.

To maximize the tax benefit, consider bundling donations into a single year so you exceed the limit, or donating appreciated stock instead of cash to avoid capital gains taxes. The savings come from reducing your taxable income, which lowers the portion of your earnings subject to tax. The higher your tax bracket, the more valuable that deduction becomes.

Bottom line

Taxes are one of the largest expenses you’ll face over your lifetime, but they’re also one of the most manageable with the right strategy. By using tools like retirement accounts, HSAs, 529 plans, and charitable giving, you may be able to reduce your taxable income today and avoid taxes on growth in the future. Small, intentional moves each year can add up to tens of thousands of dollars kept in your pocket instead of going to the government.

Related Article: How to Spend Your Tax Refund Smartly