When It Makes Sense to Swipe

Most people use a credit card without thinking much about it.

But, when should you use a credit card, really?

For groceries, gas, and online orders, it’s just another way to pay, right?.

Maybe — but knowing when you should use a card (and when you shouldn’t) can make a real difference. Used the right way, it can help you earn rewards, protect your purchases, and even potentially improve your credit score.

Used the wrong way, it can lead to interest charges, credit card debt, and financial stress.

Here’s how to use them to your advantage.

Key Takeaways

|

The Short Answer

You should use a credit card when it adds value or protection to your purchase, and if you’re confident you can pay the balance in full at the end of the month, with very few exceptions. But, more on that later.

The best use cases include everyday spending, travel, and large purchases, where you can earn rewards, benefit from fraud protection, and avoid interest charges.

1. Use a Credit Card for Everyday Purchases

Rewards add up.

Turn Routine Spending Into Rewards

Using a credit card for everyday expenses like groceries, gas, and subscriptions allows you to earn rewards, cash back, or travel points on money you’re already spending.

Why It Matters

- Earn beneficial reward points on everyday purchases

- Take advantage of cards with no or low annual fees

- Can help build a consistent credit card payment history

- Potentially help build your credit score over time

If you’re going to spend the money anyway, this is one of the easiest ways to get something back.

Related Article: The Best Credit Cards for Gas and Groceries

2. Use a Credit Card for Safer Transactions

Stronger Fraud Protection

Credit cards typically offer better fraud protection than a debit card from your bank.

If your debit card is compromised, your bank account is immediately at risk. With a credit card, the issuer’s money is at risk, not yours. However, it’s still crucial to notify the company as soon as possible.

Easier Disputes

- Unauthorized charges are easier to reverse

- You can often get a temporary credit during questionable-charge investigations

- Less immediate financial disruption

3. Use a Credit Card for Large Purchases

Built-In Protections

When making large purchases, credit cards often include:

- Purchase protection against damage or theft

- Extended warranties

- Dispute support if something goes wrong

More Control Over Payments

Credit cards can give you flexibility with time payments, but this is where caution matters.

If you don’t pay the balance in full, interest rates can quickly turn a good purchase into expensive debt.

Related Article: Best Debt Consolidation Companies This Year

Is It Ever Okay to Carry a Balance?In most cases, it’s best to pay your balance in full before the due date to avoid interest charges. But there are a few situations where carrying a balance can make sense, if you’re intentional about it. When It Can Work in Your Favor

In these cases, spreading out payments can help manage cash flow without immediately increasing costs. What to Watch Out For

The key is to stay in control. Carrying a balance should be a short-term strategy, not a long-term habit that leads to debt. |

4. Use a Credit Card for Travel

Earn Travel Rewards

Travel purchases are one of the best ways to earn rewards and travel points, especially for flights, hotels, and rental cars.

Built-In Travel Benefits

Many cards include:

- Trip cancellation or interruption coverage

- Rental car insurance

- Lost baggage protection

These benefits can add real value, often without additional cost. However, the same guidelines about paying off the balance on time still apply.

Other Credit-Card Related Articles

Check out these other reads to learn more about managing cards and their use.

- How to Budget with Credit Cards Without Going into Debt

- How to Choose a Credit Card: 7 Easy Steps

- Best Catch-All Credit Cards

- How do Balance Transfer Credit Cards Work?

- How to Consolidate Credit Card Debt

- Can Credit Cards or Personal Loans Help Pay Off Medical Debt?

- How to Use a Rewards Credit Card for Maximum Benefits

When You Should NOT Use a Credit Card

There are times when using a card can work against you.

Avoid using a card if:

- You’re likely to carry a balance

- You can only afford the minimum payment

- The purchase pushes you beyond your spending limit or credit limit

- Fees or interest outweigh the rewards

The key rule: only spend what you can afford to pay off quickly.

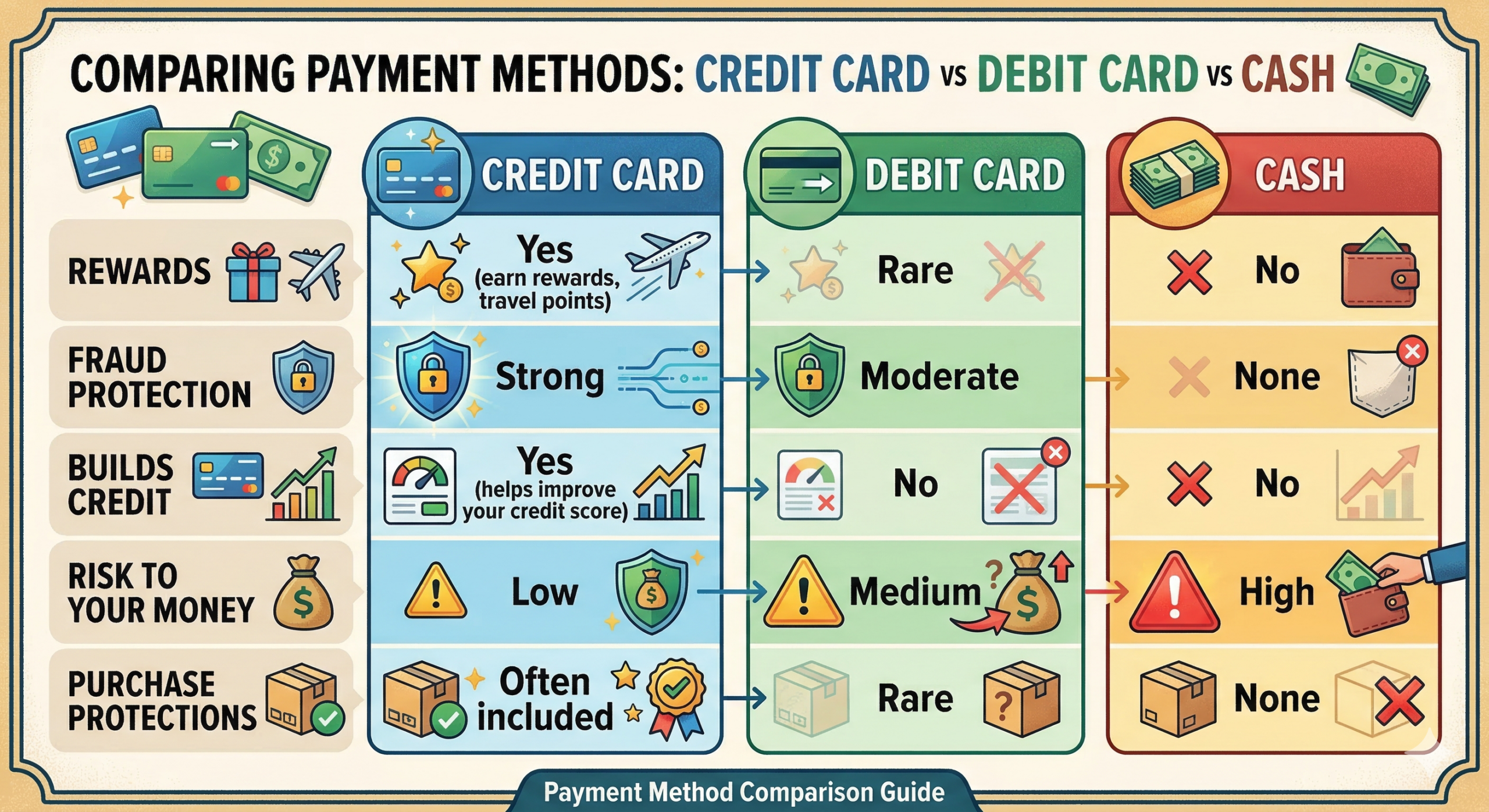

A simple comparison of credit cards, debit cards, and cash, highlighting rewards, protection, and credit-building benefits.

How to Use a Credit Card the Right Way

This is how the Federal Reserve Board lists its five tips for getting the most from your card use.

- Pay on time

- Stay below your credit limit

- Avoid unnecessary fees

- Pay more than the minimum payment

- Watch for changes in the terms of your

account

This is how you can potentially build your credit score while avoiding long-term debt.

Pro TipFrom our on-staff Certified Financial Educator For most people, having just a few cards works best. Doing so helps avoid forgotten payments or, worse yet, forgotten charges that surprise you when the bill arrives. Many people carry:

This approach helps you maximize rewards without overcomplicating things or increasing your risk of card debt. |