On the surface, there appears to be no difference between using a credit card or a debit card. You tap, swipe, or enter your information for online payments, and the transaction happens instantly.

But if you’ve ever asked, “Can I use my credit card as debit?” the answer is simple, sort of. Behind the scenes, credit cards and debit cards have very little in common. While you can use them in a similar way for many things, doing so requires a bit more discipline to avoid trouble.

Understanding how a credit card works compared to a debit card can help you avoid unnecessary interest charges, manage your line of credit, and build a stronger financial foundation over time. Here’s what you need to know.

Key Takeaways

|

Can You Use a Credit Card as a Debit Card?

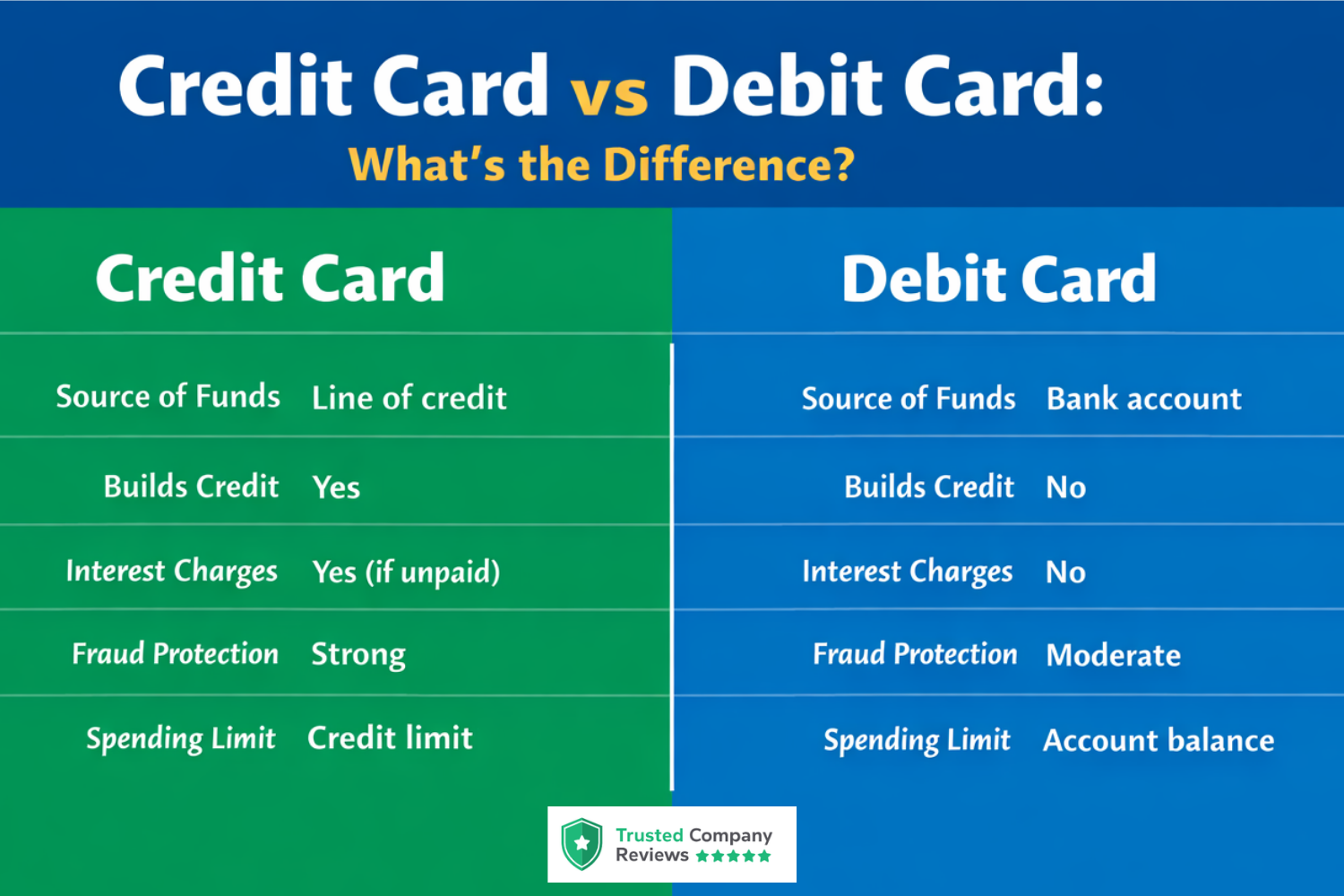

Technically, you cannot process a credit card as a debit transaction. When you select “debit” at checkout, the system pulls funds directly from your bank account.

A credit card works differently. It draws from a lender-issued line of credit, not your checking account.

That said, in everyday use, a credit card can function similarly to a debit card:

- Use for in-store purchases

- Use for online payments

- Tap, swipe, or insert at checkout

The main difference is what happens after you make the purchase.

Credit Card vs Debit Card: Key Differences

Understanding these differences can help you manage both credit and debit accounts better as well as decide how you wish to used each.

Debit Card

- Pulls money directly from your bank account

- Does not involve borrowing money

- Incurs no interest charges

- Limited to the cash you already have

- Does not help build your credit history

Credit Card

- Uses a lender-issued line of credit

- Allows you to spend now and pay later

- May include interest rates and fees

- Can help with building your credit and improving your credit scores

Check out our How to Use Credit post for more information about how credit works in general.

A side-by-side comparison showing how credit cards and debit cards differ in funding source, interest charges, and credit-building impact.

How to Use a Credit Card Like a Debit Card

While you can’t literally turn a credit card into a debit card, you can develop habits that can help make it function similarly in practice.

The primary rule to do so is simple and involves only spending money you already have available in your bank account.

Here’s how to do that:

1. Treat Every Purchase Like Cash

Before making a purchase, consider whether you would still make it if the money were immediately leaving your bank account. Doing this with every purchase can help reset your thinking about spending and also help prevent overspending.

2. Pay Your Balance in Full Every Month

Paying your full balance monthly is essential. Paying off the card more than once a month can be even better, though it’s not mandatory. Some people pay off their cards at least twice per month for easier budgeting. Carrying a balance will result in interest charges, which can quickly outweigh any rewards your card offers.

Pro TipFrom our on-staff Certified Financial Educator While debit cards are useful for controlling spending, they generally do little to help your credit scores because they don’t involve borrowing or repayment activity. Credit cards, on the other hand, can have a much greater impact on your credit profile. By using a credit card responsibly, making on-time payments, and keeping your balance low, you can actively build your credit history over time. This can help improve your credit scores and potentially allow you to qualify for better rates and financial products in the future. |

3. Track Your Spending Closely

Unlike a debit card, a credit card does not immediately reduce your bank account balance. This can make it easier to lose track of spending.

Using budgeting tools, frequently reviewing your transactions, and avoiding common budgeting mistakes can help you stay in control.

4. Use Your Card for Specific Categories

Some people limit credit card use to predictable expenses such as groceries, gas, or subscriptions. This approach helps maintain control while still allowing you to benefit from rewards and build credit.

Why People Try to Use Credit Cards as Debit

There are several reasons people prefer using a credit card over a debit card.

1. Fraud Protection

Credit cards typically offer stronger fraud protection than debit cards. Unauthorized charges are often easier to dispute, and your bank account is not directly affected.

2. Rewards and Benefits

Many credit cards, such as those listed in our overview of the best catch-all cards, offer cash back, travel rewards, or points on purchases. When used responsibly, these benefits can add value to everyday spending.

3. Building Your Credit

Using a credit card responsibly can help:

- Improve your credit history

- Increase your credit scores

- Strengthen your financial profile over time

Also Read: What Your Credit Card Says About You

The Risk: When It Stops Acting Like a Debit Card

The biggest risk with using a credit card is that you’re not really using your own money at the outset. Credit card money is, after all, borrowed money.

If you:

- Spend more than you can afford

- Carry a balance month to month

- Miss payments

You may face:

- High interest rates

- Growing interest charges

- Long-term debt

Can You Pay Bills With a Credit Card?

Many people assume they can use a credit card for all expenses, including major bills. In reality, this is not always practical.

Some lenders and service providers:

- Don’t accept credit card payments at all, or

- Charge processing fees, typically between 2% and 3%, which outweigh most benefits from any potential rewards earned for the transaction

Common Examples:

- Mortgage payments

- Rent payments

- Utility bills

- Loan payments

Even when credit cards are accepted, the fee can outweigh any rewards earned.

For example:

- A 2% cash-back reward

- A 3% processing fee

This results in a net loss.

In most cases, using a credit card for bills only makes sense if there is no fee or if you have a short-term plan to pay the balance off immediately.

Alternatives to Using a Credit Card Like a Debit Card

If you prefer the safety of a debit card but want more flexibility, there are several alternatives.

- Prepaid Cards: These cards are loaded with funds in advance and allow you to spend only what you have deposited.

- Cash-Back Debit Cards: Some debit cards offer rewards while still limiting spending to your bank account balance.

- Budgeting Systems: Structured budgeting methods, such as category-based spending limits, can help you maintain control without relying heavily on credit.

When It Makes Sense to Use a Credit Card

A credit card can be a useful financial tool when:

- You consistently pay your balance in full

- You want added fraud protection for purchases

- You are working on improving your credit

- You are earning rewards for money you were already going to spend anyway