Over 110 Million Americans Can’t Pay Their Credit Card Bills – Here’s What You Need To Know

More than 110 million Americans can’t pay their credit card bills in full as debt surpasses $1 trillion and interest rates remain elevated.

Many Americans are struggling to keep up with rising credit card balances and interest rates.

Image enhanced by AI

Americans continue to fall deeper into debt as the latest consumer advocates say 111 million Americans can’t pay their credit card bills in full.

What’s more, this isn’t siloed to those with lower household incomes. Federal Reserve Data suggest that those in the upper-middle and upper-income classes are equally reliant on credit to get by. Even celebrity Ray J is being pursued by American Express for $78,000 of unpaid debt.

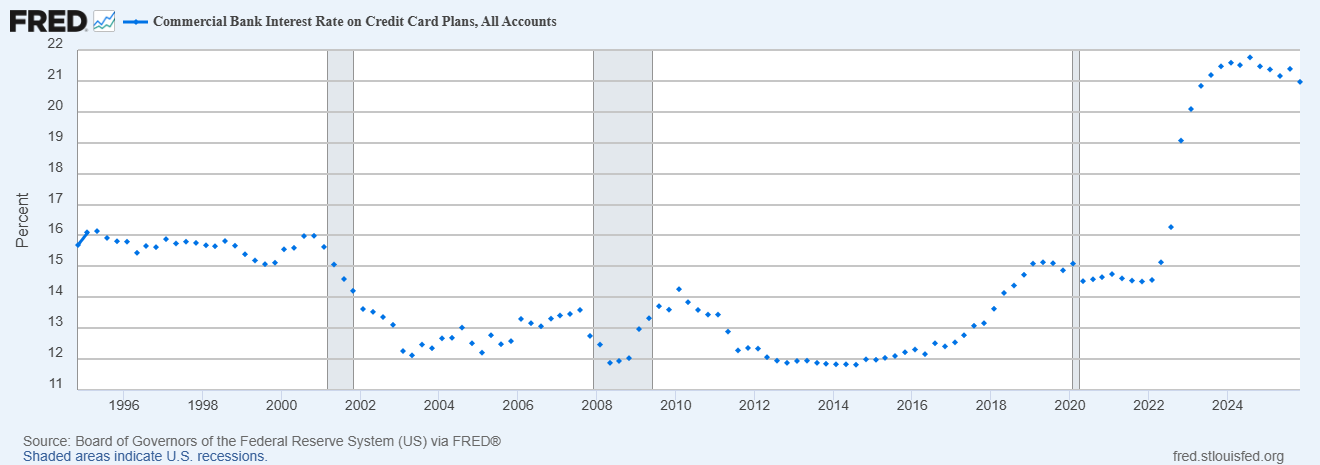

This has amounted to over $1 trillion in total consumer debt held as reported by the Federal Reserve Bank of St Louis. At an average 21% interest rate, this is a massive issue that has the White House’s attention.

Here’s what you need to know, and resources to support your own debt payoff journey.

Why Credit Card Debt Is So Dangerous Right Now

Credit card debt is the financial slippery slope that millions of Americans find themselves on – but it’s especially more dangerous today than in the past.

First, interest rates have rocketed in recent years. Since the rise of inflation in 2022, interest rates have risen from 15% up to 22%. Some credit card rates are even higher.

Average credit card interest rates have climbed above 20%, making it harder for millions of Americans to keep up with balances. Source: Board of Governors of the Federal Reserve System (US), via FRED (Federal Reserve Economic Data)

Part of President Trump’s political campaign leading up to the 2024 election was capping interest rates at 10% on credit card companies for one year. This hasn’t come to fruition, while Americans have paid a total of $240.7 billion in credit card interest charges since January 2025, according to The Century Foundation.

Mix this with millions living paycheck to paycheck and rising unemployment, and it’s leading to more people relying on credit cards to make ends meet. In fact, more than half (55%) say they now use credit cards for everyday expenses. And with a large swath of those not paying their statements in full, it’s creating a debt spiral that many may not be able to escape.

What Happens If You Fall Behind

If you keep up with your credit card bills, paying on time, you’ll likely avoid interest penalties. This is akin to flushing money down the toilet.

However, if you fall behind on payments, this is where things can become worse. Here’s what the timeline could look like.

Day 1–29 (Missed payment):

You’ll likely be hit with a late fee, but your issuer typically won’t report the missed payment to credit bureaus yet. This is your window to fix it with minimal damage.

Day 30:

The account becomes officially delinquent and is reported to credit bureaus. This is when your credit score takes its first real hit. A LendingTree study found that missing one payment could amount to an 80-point loss.

Day 60–90:

Additional late fees stack up, penalty APRs may kick in, and issuers may begin calling more aggressively. You may start receiving frequent calls or letters. The balance can grow quickly here due to compounding interest and fees, making it harder to catch up.

Day 120–180:

At this point, the account is severely delinquent. Lenders may restrict or close your account entirely.

Around Day 180:

The account is typically charged off (more on that below) and either sent to internal collections or sold to a third-party debt collector. You’ll likely begin hearing from third-party collectors, and the account may appear on your credit report as both a charge-off and a collection.

Also Read: Mortgage Help Searches Surge to Record High as Homeowner Stress Grows

How To Tackle Credit Card Debt, Today

If you find yourself sliding into, or already in, credit card debt, the first thing to recognize is that you aren’t alone. Millions are in your same position, and there is a pathway to eliminating credit card debt.

Here are the basic steps and strategies to start climbing out from this financial predicament:

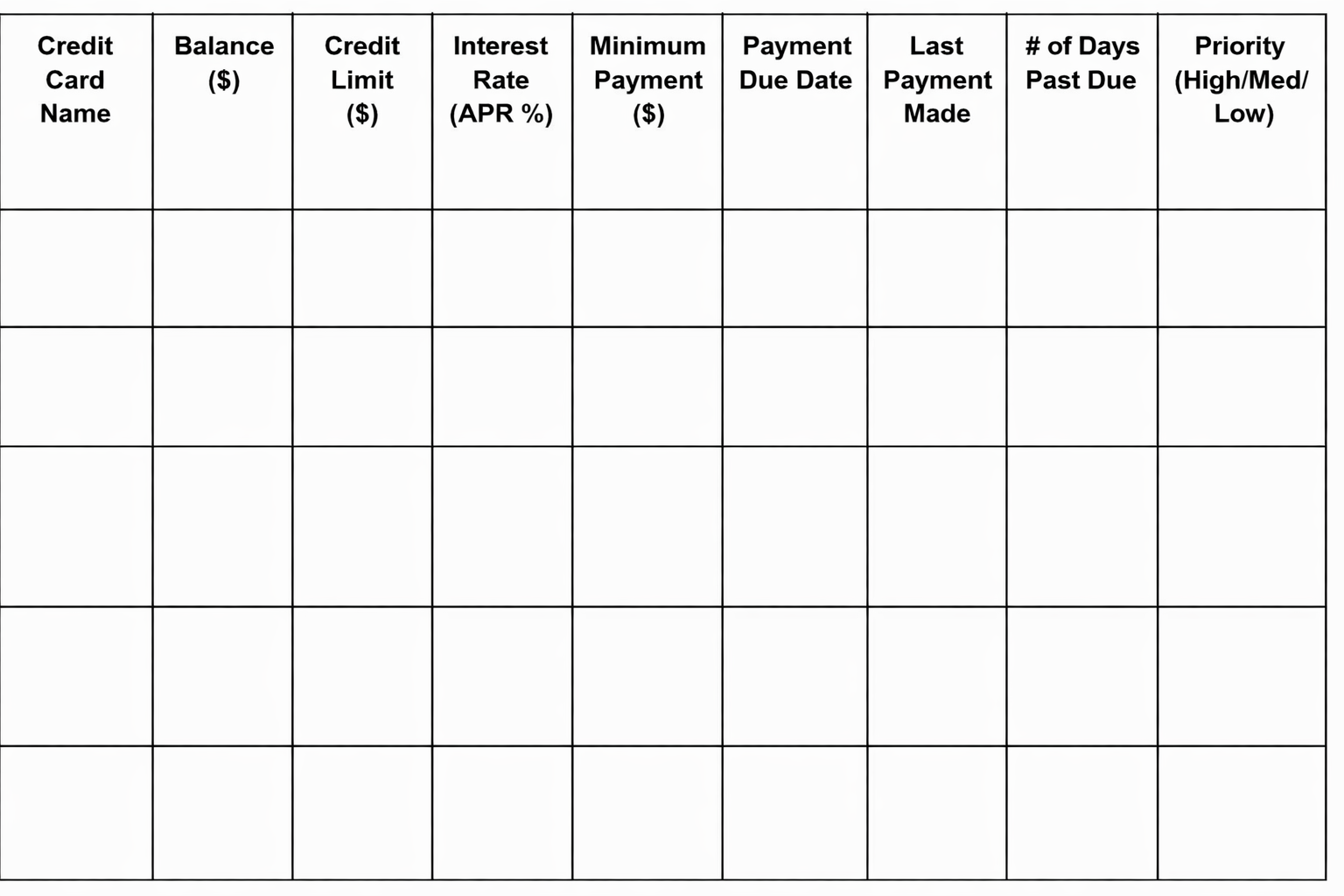

List out all of your debts

There’s something psychological about putting a pen to paper and visualizing everything in front of you. List out your debts in a chart similar to this:

A simple worksheet to organize your credit card balances, interest rates, and payment priorities.Doing this will help you put together your total debt, which cards you need to prioritize paying off first, and build a mental runway to begin tackling it.

Tools to Help You Take the First Step

Trusted Company Reviews offers a collection of financial calculators designed to help you take control of your credit card debt. Use these tools to break down your balances, explore repayment options, and build a plan that works for your situation.

- Personal Loan Calculator

- Debt Consolidation Calculator

- Home Equity Loan Calculator

- Debt Snowball Budget Calculator

- Monthly Budget Calculator

- Auto Loan Refinance Calculator

- Cash-Out Mortgage Refinance Calculator

Find a raise to way your income, or side hustle

There’s a clear rule in personal finance: you can only cut back so much, but you can make an unlimited amount of money.

Yes, it’s always a good idea to cut back on unnecessary spending through budgeting and redirect those funds to paying off high-interest debt. But asking for a raise, switching jobs for a higher income, or using cash windfalls like your 2025 tax refund can be a much more fruitful way to knock down your credit card debt.

Crush your interest rates first

The principal amount you have may be a burden, but the mounting interest is likely the real problem – especially with average rates above 20% APR.

There are a few ways you can get these rates down quickly:

- Use a balance transfer credit card: There are credit cards available that aim to help consumers with revolving credit card debt. You can move your balance from your current card with a high interest rate to one with a promotional lower rate. The terms differ from card to card, but you can potentially move your debt from a card with a high interest rate to one with 0% APR for many months.

- Consider a personal loan: There are personal loans available for you to pay off your current credit card debt, and allow you to work on one large balance. However, interest rates will vary between lenders, so be sure to shop around.

- Consider debt consolidation: Similar to personal loans, you can bring multiple debts under one roof and begin knocking them down.