Credit can be one of the most useful financial tools available. But only if you know how to use it correctly. When used wisely, credit can help you build your credit score, finance major purchases, and manage cash flow over time. When misused, it can lead to high interest charges, growing debt, and long-term financial stress.

While some fear it and simply avoid the topic altogether, understanding how to use credit is about learning how to make it work for you instead of against you. Here’s what you need to know.

Using credit responsibly means knowing which financial tools fit your situation and when it’s time to consider a different approach. If high-interest unsecured debt has become difficult to manage, learning more about Accredited Debt Relief can help you evaluate whether a debt solution is a better fit than continuing to rely on revolving credit.

Key Highlights

|

What It Means to Use Credit

Using credit means borrowing money now with the agreement to repay it later, often with interest. A credit card company or lender extends you a credit line, which is the maximum amount you can borrow at any given time.

Common forms of credit include:

- Credit cards

- Personal or unsecured loans

- Secured loans (mortgages, automobiles)

- Student loans

- Home equity loans or lines of credit

- Refinancing loans

- Buy now pay later (BNPL) financing

- Payday loans

When you use credit, you’re essentially getting access to funds upfront and paying them back over a defined period of time. You’ll typically be charged interest based on current interest rates, and failure to make scheduled payments or repay the full amount can have serious negative impacts on your credit report and score.

That’s why credit isn’t free money. It’s a tool. And, it’s one that can either help or hurt your financial situation, depending on how you manage it.

Related Article: What Your Credit Card Says About You and About Your Finances

How to Use Credit Cards Responsibly

Credit cards are one of the most common ways people use credit, and they’re also one of the easiest ways to get into trouble if not handled carefully. Learning to use credit cards responsibly is one of the most important steps in building a strong financial foundation.

The Consumer Financial Protection Bureau describes credit cards this way:

| “An open-ended loan that allows you to borrow money up to a certain limit and carry over an unpaid balance from month to month. There is no fixed time to repay the loan as long as you make the minimum payment due each month. You pay interest on any outstanding credit card loan balance.” |

Start by always making at least the minimum payment by the due date. Missing payments or paying late can hurt your credit score and trigger additional fees. But while the minimum payment keeps your account in good standing, it doesn’t prevent interest charges from building up.

The best approach is to pay your full balance each month whenever possible. Doing this helps you avoid paying interest entirely, making your credit card a convenient payment method rather than a source of debt.

It’s also important to monitor your balance each month and stay well below your credit limit. Keeping your spending under control helps maintain a healthy credit utilization ratio, which plays a major role in your credit score.

Used properly, credit cards can help you build your credit score, earn rewards, and provide financial flexibility without leading to long-term debt.

Related Article: Can I Use My Credit Card as Debit? What to Know Before You Try

How Credit Affects Your Credit Score

Your credit score is a numerical representation of how reliably you use credit. Lenders use it to determine your eligibility for loans, interest rates, and credit limits. Your automobile and homeowners’ insurance rates, as well as things like how much car you can afford, can also be impacted by your credit score.

One of the most important factors in your score is your history of making payments on time. Even one missed payment can have a negative impact, while consistent on-time payments help build your credit score over time. Tier one credit-score holders often set up autopay to ensure timely payments each month, just to be sure.

Another key factor is your credit utilization ratio, which compares how much of your available credit line you’re using. For example, if your credit limit is $10,000 and your balance is $3,000, your utilization ratio is 30%. Lower utilization is generally better and signals responsible use of credit.

Other factors include the length of your credit history, the types of credit you use, and how often you apply for new credit. Together, these elements determine how lenders view your financial behavior and risk level.

Improving your credit comes down to consistent habits, including paying on time, keeping balances low, and using credit strategically.

Pro TipFrom our on-staff Certified Financial Educator If you have older credit card accounts that don’t charge annual fees, keep the accounts open, even if you don’t use them. However, you’ll have to use them from time to time to avoid non-use closure. Doing this can result in a longer average credit history, which can help strengthen your credit profile, and keeping these accounts active also increases your total available credit, which can help keep your credit utilization ratio down. |

How to Use Different Types of Credit

Not all credit works the same way. Understanding how different types of credit function can help you use them more effectively.

Personal Loans and Monthly Payments

Personal loans provide a lump sum of money that you repay over time through fixed monthly payments. These loans typically come with set interest rates, making it easier to budget.

They can be useful for large expenses, but it’s important to understand how much you’ll pay in interest over the life of the loan.

Using Debt Consolidation Wisely

Debt consolidation combines multiple debts into one loan or balance transfer, often with a lower interest rate. This can simplify payments and reduce the total amount of interest you pay.

For example, some credit cards offer balance transfer promotions that allow you to move existing debt and pay it off with little or no interest for a limited period of time.

However, consolidation only works if you avoid taking on new debt while paying off the old balances.

Mortgages and Car Loans

Mortgages and auto loans are longer-term forms of credit used to finance major purchases. These loans typically involve fixed monthly payments over several years.

Because of their size and duration, they can have a significant impact on your credit profile. Making payments on time consistently helps strengthen your credit, while missed payments can have serious consequences.

Common Mistakes to Avoid When Using Credit

Even with good intentions, it’s easy to misuse credit. Avoiding these common mistakes can help protect your finances.

- Only making the minimum payment: This keeps you in debt longer and increases the amount of interest you pay.

- Missing the due date: Late payments can damage your credit score and result in fees.

- Carrying a high balance: High balances increase your credit utilization ratio and make debt harder to manage.

- Maxing out your credit limit: This signals risk to lenders and can lower your credit score.

- Opening too many accounts in a short time period: Frequent applications can negatively affect your credit.

Recognizing these pitfalls early can help you make better financial decisions.

Keep in MindFrom our on-staff Certified Financial Educator Be mindful of hard inquiries when applying for new credit. Each application can result in a hard inquiry on your credit report, which may temporarily impact your score and affect approval decisions, even if you have otherwise strong credit. Hard inquiries typically remain on your credit report for two years, though their impact tends to lessen somewhat over time. Limiting unnecessary applications can help protect your credit profile and help minimize rejections due to “too many hard inquiries.” |

Related Article: What to Look for in the Most Trusted Review Sites

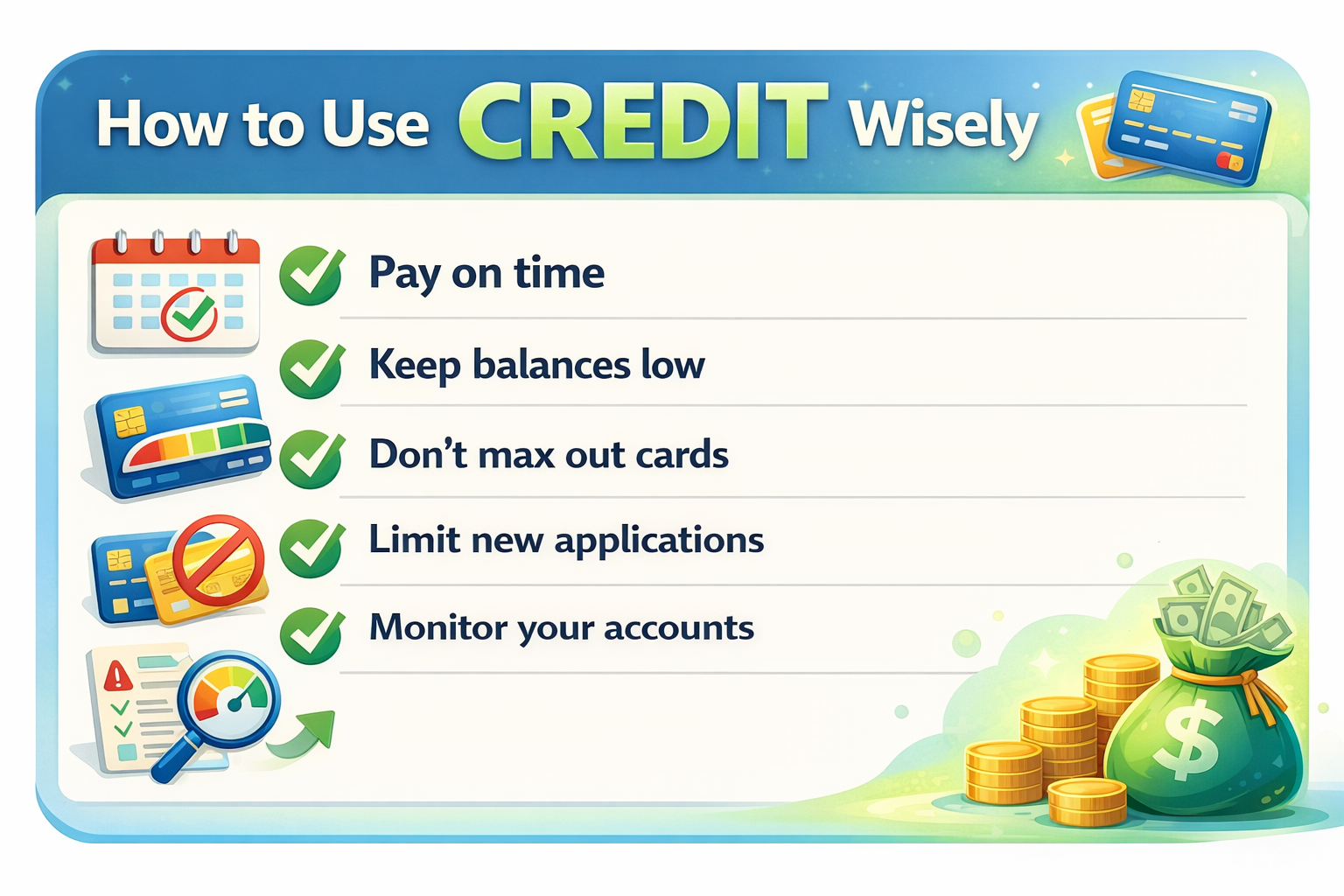

Simple Tips for Improving Your Credit Over Time

Improving your credit doesn’t require complicated strategies. It’s about consistency and discipline.

- Pay all your bills on time, every time

- Keep your balances low relative to your credit limit

- Pay your balance each month whenever possible

- Avoid unnecessary debt and multiple new credit applications

- Monitor your accounts regularly for accuracy and fraud

Over time, these habits can significantly improve your credit and open the door to better financial opportunities.

Simple tips for how to use credit wisely and build strong financial habits

Related Article: How to Find Extra Money in Your Budget

When Credit Works for You (And When It Doesn’t)

Credit works best when you use it intentionally. It can help you manage large purchases, smooth out cash flow, and build a strong financial profile. However, credit is problematic when it’s used to try to replace income or support an unaffordable lifestyle. Relying on credit without a repayment plan often leads to long-term debt and financial stress.

The goal use credit as a tool that supports your financial goals rather than undermines them.

Related Article: How Late Can You Be on a Car Payment Before You Lose Your Car?