Key Takeaways

|

Most car loans include a grace period of 10 to 15 days before late fees apply, but missed payments hit your credit at 30 days late, and your lender can technically begin repossession after a single missed payment, depending on your state and loan contract. How late you can really be on a car payment without serious consequences depends on your lender’s grace period, your state’s repossession laws, and how quickly you reach out about hardship.

If you’re struggling to keep up with your car payment because of mounting credit card balances, medical bills, or other unsecured debts, exploring available debt solutions may help you create more room in your monthly budget. Learning more about Accredited Debt Relief can help you determine whether a debt solution could help you avoid falling further behind on important financial obligations.

This guide walks through the timeline of consequences at each stage, addresses your real legal protections, and examines practical steps that keep your car and protect your credit.

Related Article: What Happens If I Can’t Pay My Mortgage?

How Late Can You Be on a Car Payment Before Late Fees?

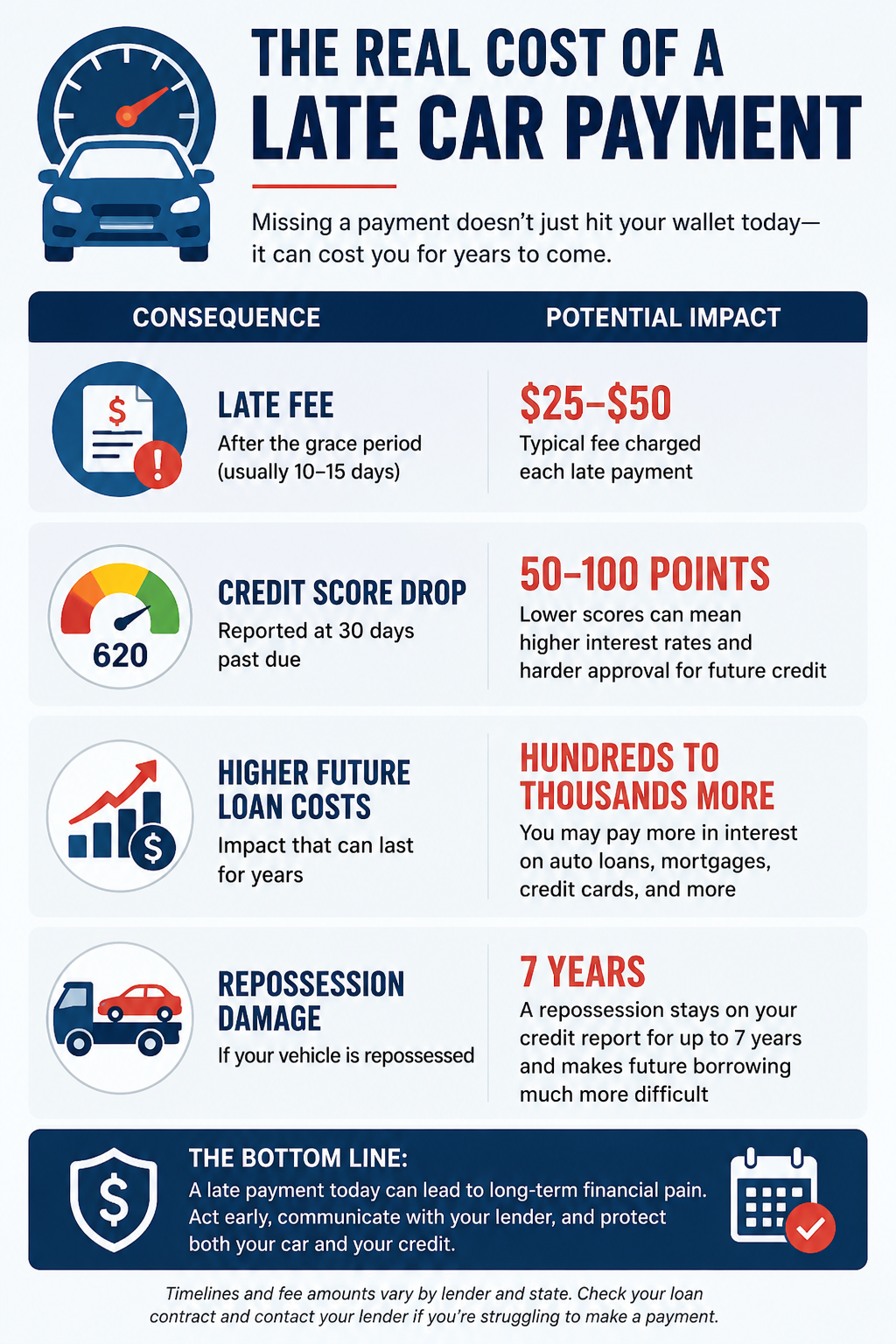

Most car loans include a 10 to 15-day grace period before any late fee applies. After that grace period, lenders typically charge a late fee equal to 5% of the payment or $25 to $50, depending on the loan agreement. Catching up before day 10 to 15 typically resets the situation completely without affecting your credit or triggering a fee.

Related Article: Late Car Insurance Payment? What Happens and How to Avoid Cancellation

How Many Days Can You Be Late on a Car Payment Before Each Consequence?

Knowing exactly when each consequence will happen helps you decide where to act and how urgently.

This is the typical timeline:

| Days Late |

What Happens |

| 1 to 10 (grace period) | No late fee, no credit reporting. Catching up resolves the situation completely. |

| 10 to 15 | Late fee charged, typically 5% of the payment or $25 to $50. Credit reporting has not started. |

| 30 | The lender reports the missed payment to credit bureaus. Credit score may drop 50 to 100 points. |

| 60 | A second missed payment is reported. The lender may begin pre-repossession outreach. |

| 90+ | The lender may move to repossess the vehicle. State laws vary on timing. |

According to the New York Fed’s Household Debt and Credit Report, auto loan delinquencies have risen significantly in recent years, reaching levels not seen since the aftermath of the 2008 financial crisis.

Related Article: What Happens if I Don’t Pay a Collections Agency?

When Can a Lender Repossess Your Car?

Repossession laws vary by state. However, the legal threshold can be surprisingly low across the spectrum. The Consumer Financial Protection Bureau reports the share of vehicle loans assigned to repossession is now well above pre-pandemic levels. This reflects both higher car prices and weaker borrower budgets.

In most states, the lender’s contract reserves the right to repossess the vehicle after the borrower misses just a single payment. However, most lenders would rather work with the borrower before they resort to repossession.

Repossession laws are addressed in state laws, and include notice requirements, peaceful repossession rules, and your right to redeem the vehicle. This means that the practical experience varies even where the legal thresholds are similar.

How a Late Car Payment Affects Your Credit Score

Once your car payment is 30 days past due, the lender may report it to the credit bureaus. That can lower your credit score by 50 to 100 points, depending on your overall credit profile. Even if you catch up on the payments, the late-payment mark can remain on your credit report for up to seven years.

If your account reaches the level of repossession, your credit damage compounds. The repossession itself appears as a separate negative event and stays for seven years, making it significantly harder to qualify for another auto loan, mortgage, or unsecured credit during that time.

Missing a car payment can trigger late fees, credit score damage, higher future borrowing costs, and even repossession if the situation continues long enough.

What to Do If You’re Late on a Car Payment

The earlier you act, the more options you can retain.

Contact Your Lender First

If you’re having trouble making your car payment, it’s worth contacting your lender as early as possible. Banks and credit unions often offer deferments, hardship assistance, or modified payment plans. Taking back a vehicle is expensive and time-consuming for lenders, so they’re often more willing to work with borrowers than people expect.

Refinance Your Auto Loan

If your monthly payment no longer fits your budget, refinancing your auto loan can reduce the payment and free up monthly cash. Pre-qualifying with multiple lenders takes a few minutes and shows your real options without affecting your credit. You can compare current refinance options in our review of the best auto refinance loan providers or estimate your potential savings using our auto loan refinance calculator.

Address the Broader Debt Picture

A late car payment is often a deeper signal of pressure within the household budget. If credit card balances, medical bills, or other debts are taking their toll on your budget, a debt consolidation loan can combine many of those into a single lower monthly payment, potentially freeing up room, simplifying your budget, and potentially helping you to help keep the car payment up to date.

Related Article: Credit Card Debt Is Soaring. Here’s How You Can Escape It

Further Reading

- Debt Consolidation with Bad Credit: What to Expect and How to Qualify

- Alternatives to Bankruptcy: Try This Option First

- Credit Card Debt Is Soaring. Here’s How You Can Escape It

- Millions of Car Owners Face Late Car Payment Difficulties

- How Late Can You Be on a Car Payment Before You Lose Your Car?

- Credit Card Debt Forgiveness: What’s Real and What’s a Scam

- Best Debt Consolidation Companies of the Year