Key Takeaways

|

Bundling home and auto insurance combines both policies under one carrier to potentially realize multi-policy discounts of 10% to 25% on the combined premium, while also streamlining billing, claims, and customer service.

The biggest benefit to the insured is cost savings. However, bundling also reduces administrative processes for the insurance company and can simplify claims when a single event affects both your home and your vehicle. Whether it’s the right move for you depends on how your bundled quotes compare to your best standalone options.

Understanding what bundling actually changes, and where it falls short, is the best starting point before switching carriers or consolidating policies.

Why Do Consumers Bundle Home and Auto Insurance?

Consumers usually bundle their home (or renters) and auto insurance policies to lower their combined premiums. Doing so helps simplify how you manage your policies, and can provide access to discounts that aren’t always available on standalone policies.

The most common reasons for bundling include:

- Cost savings from a multi-policy discount applied to one or both policies.

- Single billing and account management instead of having separate insurers.

- Easier claims handling when one event affects both the home and vehicle.

- Potential access to loyalty rewards and longevity benefits.

When Does Bundling Insurance Make Sense?

John Espenschied, Agency Owner at Insurance Brokers Group, puts it this way, “Bundling usually makes sense if both policies are competitively priced on their own and you are getting a real multi-policy discount in the 10 to 25 percent range. It is especially helpful for families with a house, multiple cars, maybe a teen driver, and an umbrella policy. Where it fails is with high-risk drivers or unusual homes, where only a few carriers will even write the policy. In those cases, mixing companies is often cheaper.”

How Much Can You Save by Bundling Home and Auto Insurance?

Most households save between 10% and 25% on combined home and auto premiums when they sign up with a single carrier to bundle policies. However, actual savings vary by insurer, state, and your individual risk profile.

According to the Insurance Information Institute, multi-policy discounts are one of the most consistent ways to reduce combined home and auto premiums.

Typical Bundle Savings by Carrier Tier

| Carrier Tier | Typical Bundle Savings* |

| High-discount bundles | Up to 25% |

| Mid-tier bundled | 10% to 20% |

| Lower-discount bundles | Up to 13% |

| Industry average | Roughly 15% |

*Savings vary by state, insurer, and individual risk profile. Compare bundled and standalone quotes to confirm actual savings.

Some insurers apply the bundling discount to both policies, while others apply most of the savings to one half of the bundle. Ask your insurer how it distributes any discounts to help confirm where the value actually lands.

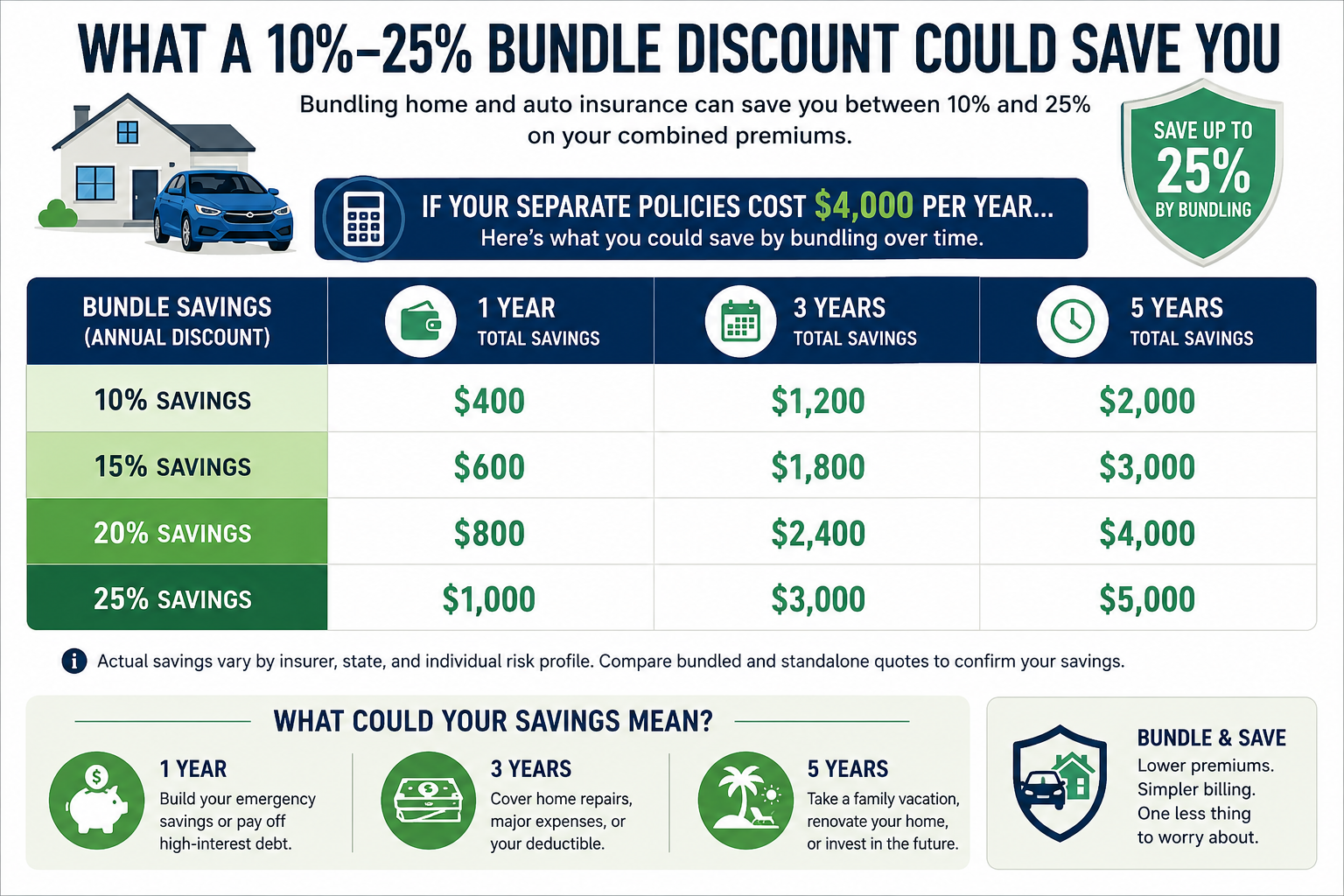

What a 10%–25% Bundle Discount Could Save You

See how bundling home and auto insurance can reduce your costs over time — and what those savings could look like over one, three, and five years.

Bundling home and auto insurance can save many households thousands of dollars over time, depending on the carrier and discount level.

What’s Typically Included When You Bundle?

Bundling combines your home and auto policies under one carrier without changing your coverage levels. The policies remain separate but linked for discount and account purposes.

A typical bundle includes:

- A multi-policy discount that applies to one or both premiums.

- Unified billing with a single payment schedule.

- A single online account or app for both policies.

- One agent or service team handling both lines of coverage.

- Potential for a combined deductible when one event triggers claims on two or more policies.

How Does Bundling Simplify Claims?

Bundling simplifies the claims process by routing both your home and auto claims through one insurer. A single adjuster can often handle overlapping events.

Simplification through bundling matters most when a single event, such as a fallen tree, a storm, a fire, or a break-in, damages both your home and your vehicle. When you have a single carrier, you can likely file your claim once, talk to a single adjuster, and may only owe one deductible, if your carrier and the policy include that feature.

What Other Discounts Can Stack With a Bundle?

Bundle discounts typically stack with other savings programs that the insurer offers for auto, home, or both. The most common stackable discounts include:

- Telematics programs that track driving behavior (Drive Safe & Save, Drivewise, SmartRide, IntelliDrive, Signal).

- Safe driver and accident-free discounts on the auto half.

- Protective device discounts for home alarms, smoke detectors, and smart sensors.

- Paperless billing, autopay, and loyalty discounts for both policies.

- Multi-vehicle and good student discounts for the auto side.

When Is Bundling Home and Auto Insurance NOT a Good Idea?

Bundling isn’t a good idea when a specialist insurer prices your home or auto policy significantly lower than a bundler’s combined rate. The math doesn’t always favor bundling.

Bundling May Not Save You Money If:

- Your standalone auto premium is significantly lower than it would be with a non-bundled policy.

- Your home risk profile triggers significantly high premium rates.

- You hold specialty coverage (classic car, high-value home) that bundlers can’t match or don’t offer.

- You frequently switch carriers.

- The carrier sells one policy as an affiliate rather than direct coverage.

Comparing both bundled and standalone quotes side by side is the only reliable way to confirm whether bundling actually saves you money.

Does Bundling Affect Your Insurance Rates After a Claim?

Filing a claim on one half of a bundled policy typically doesn’t raise the rates of the other, because home and auto policies are rated separately, even when bundled with the same carrier.

For example, if you have a roof claim on your home policy, it generally won’t increase your auto premium. However, having multiple claims on both policies may eventually affect your overall standing with the carrier. This could influence your renewal pricing or eligibility.

How Do You Choose the Right Bundle?

To choose the right home and auto bundle for you, start by gathering bundled and standalone quotes from at least three carriers, then weighing total cost, claims service, and add-on availability.

- Get bundled quotes from at least three carriers operating in your state.

- Also, gather standalone home and auto quotes for direct comparison.

- Compare the total combined annual premium, not just the discount percentage.

- Check claims satisfaction ratings from J.D. Power and the Better Business Bureau.

- Confirm which add-ons and telematics programs stack with the bundle discount.

For a side-by-side comparison of the top carriers, including savings potential, coverage flexibility, and which bundle fits different household priorities, see our review of the best home and auto insurance bundles.

Compare the Top Home and Auto Insurance Bundle ProvidersIf you’re ready to start comparing options, these resources can help you evaluate the top carriers side by side:

Each review covers savings potential, coverage flexibility, telematics programs, and who each carrier fits best. |