Falling behind on a credit card payment is stressful, but panicking won’t help. On the other hand, understanding the consequences will. Whether you’re short on cash this month or dealing with a longer stretch of financial hardship, knowing exactly what happens, and when, gives you the power to act before the situation gets worse.

If you’re finding it difficult to keep up with your credit card payments, exploring professional debt solutions early may help you avoid more serious financial consequences. Learning more about Accredited Debt Relief can help you understand whether a debt solution or other approach makes sense for your financial situation.

Here’s a clear breakdown of what happens when you can’t pay your credit card bill and, more importantly, what your real options are.

Key Takeaways

|

How Credit Cards Work

Your card runs on a monthly billing cycle. At the end of each cycle, your credit card company sends a statement with your balance and a minimum payment due. You have a grace period (usually 21 to 25 days) before interest kicks in.

Carrying a balance means interest accrues daily based on your APR. The minimum payment keeps you current, but paying only that is the slowest and most expensive way to reduce credit card debt.

What Happens When You Stop Paying

Days 1–29

When you miss a payment, your provider will immediately charge a late fee, which is usually between $25 and $40. A penalty APR may also kick in. However, your credit score won’t be affected yet, as credit bureaus don’t receive a delinquency report until your account is 30 days past due. There’s still time to act.

30 Days Past Due

Your credit card company reports the missed payment to the credit bureaus. Since payment history makes up 35% of your FICO score, the impact on your score can be significant. Many in this situation see quick drops of between 50 and 100 points.

60–90+ Days Past Due

At this stage, your account may be charged off and the credit card debt sold to a collections agency. Legal action and wage garnishment become real possibilities. The credit damage is severe and can follow you for up to seven years.

Your Options When You Can’t Afford to Pay

Call Your Credit Card Company First

This is the most important step. The CFPB recommends contacting your issuer as soon as you think you might miss a payment. Many credit card companies offer hardship programs, temporary rate reductions, or payment deferrals, but each lender is different, and you’ll have to ask.

Pay at Least the Minimum

If you can manage it, making the minimum payment stops the 30-day clock and keeps your account in good standing. It won’t reduce your credit card debt much, but it protects your credit score while you work through the situation.

Consider a Balance Transfer

If you can transfer your balance to a 0% intro APR card, it pauses interest and gives you breathing room to pay down credit card debt without it growing. This works best if your credit score is still intact.

Transferring your balance to a 0% intro APR card pauses interest and gives you breathing room to pay down credit card debt without it growing. This works best if your credit score is still intact.

Look Into Debt Consolidation

If you’re juggling multiple credit card bills, you may be able to use debt consolidation to roll them into one loan, often at a lower rate.

Related: What is Debt Consolidation?

Try Nonprofit Credit Counseling

Agencies affiliated with the National Foundation for Credit Counseling (NFCC) can negotiate reduced rates with your creditors and set up a debt management plan for your credit card bills.

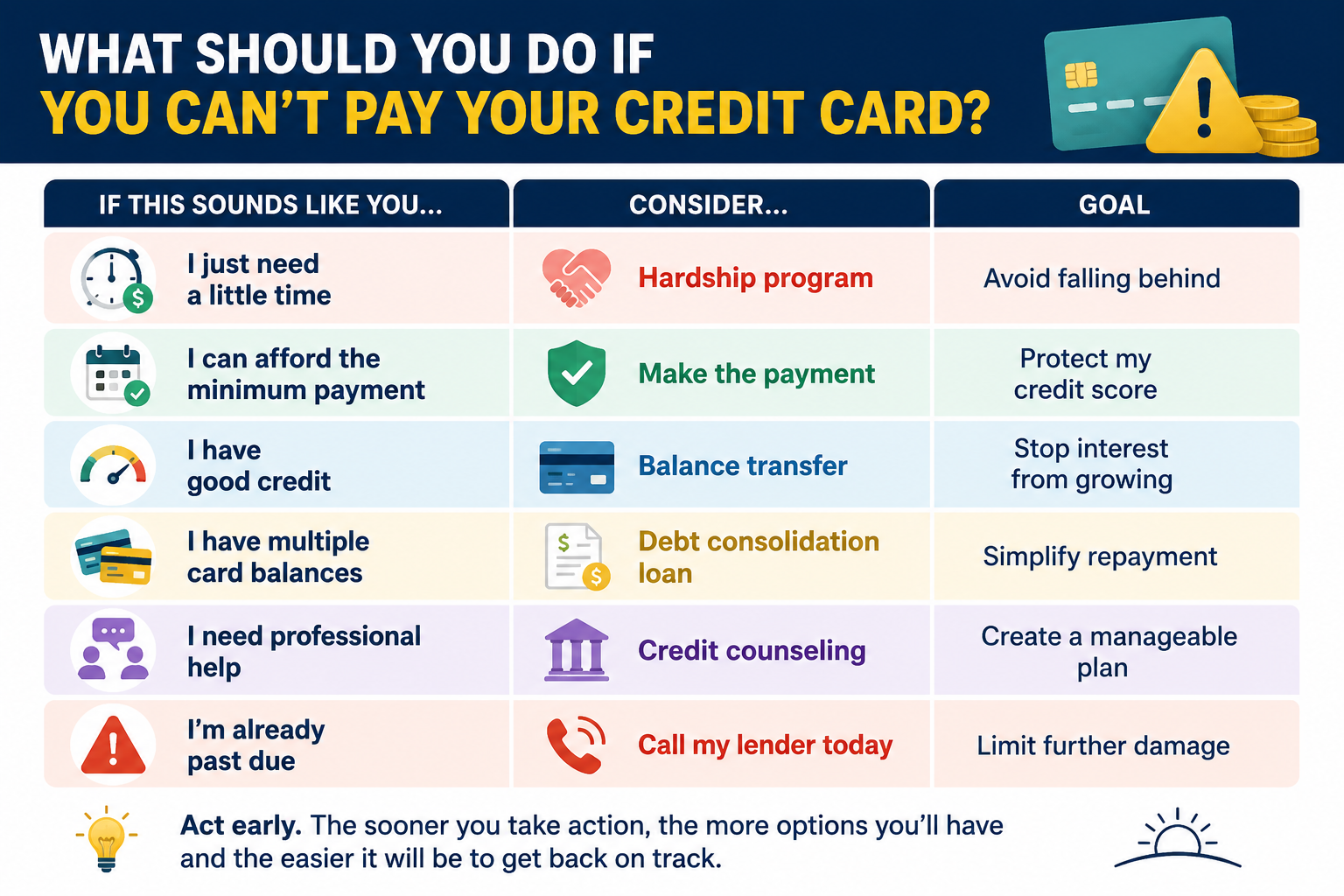

If you’re struggling to pay your credit card bill, the right solution depends on your situation. This infographic highlights five practical options that may help you avoid credit damage, reduce interest costs, and regain control of your finances.

How to Recover After Missing Payments

Getting back on track takes time, but it’s doable. Start by catching up on past-due credit card bills as quickly as possible. The damage to your credit score will stop getting worse once you can make your account current again.

Pro TipWe asked Professor Mary Sasmaz, Assistant Professor in the Department of Accountancy at Case Western Reserve University, for her thoughts on catching up after missing payments… If you are only able to make the prior-statement payment, then you should expect interest charges on the next month’s bill and should be able to restore the no-interest grace period within a couple of months, as long as you are making full payments. If there is a good reason for the late payment (hospitalization, banking issue, something else), some credit card companies are willing to waive a late payment fee. Sometimes they are even willing to waive the fee as a courtesy for long-term loyalty, but they don’t have to and won’t do it regularly. It’s worth a call to ask. After getting current, it’s worth a thought about whether setting up credit card payments for autopay makes sense for you. Just be sure to review your statement every month, even if it’s autopaid, to monitor for any fraudulent activity. |

Going forward, keeping a closer eye on your monthly cash flow with a budgeting app can help you catch a shortfall before it becomes a missed payment. Simple, basic, and free versions are available through several providers.

Related: What Happens If I Can’t Pay My Mortgage?

Further Reading

- Debt Consolidation with Bad Credit: What to Expect and How to Qualify

- Alternatives to Bankruptcy: Try This Option First

- Credit Card Debt Is Soaring. Here’s How You Can Escape It

- Millions of Car Owners Face Late Car Payment Difficulties

- How Late Can You Be on a Car Payment Before You Lose Your Car?

- Credit Card Debt Forgiveness: What’s Real and What’s a Scam

- Best Debt Consolidation Companies of the Year

- What Happens If I Can’t Pay a Judgment?