If you can’t pay a judgment, the creditor can take additional steps to collect the debt.

Creditors may use enforcement tools such as wage garnishment, bank account levies, or property liens, depending on your state’s laws. However, a judgment against you does not mean you are out of options.

If you’re worried about how you’ll pay a judgment or manage other overwhelming debt, it’s important to understand all of your options before collection efforts become more aggressive. Learning about professional debt solutions, such as Accredited Debt Relief, can help you determine whether negotiating or resolving unsecured debt is a realistic path forward.

Here’s what you need to know about judgments and your possible options.

Key Takeaways

|

What Is a Judgment?

A judgment is a court order stating that one party legally owes money to another. While you can owe a debt without a judgment, a judgment only exists after a creditor files a lawsuit and a court rules in their favor. Once a judgment is declared, the court has formally determined that the debt is valid and owed.

The judgment document serves as the official record of the court’s decision. The document identifies the parties involved, the amount owed, court costs or interest, and other case-pertinent information.

Small claims court and civil court can issue judgments. Small claims courts generally handle lower-dollar disputes, while civil courts handle larger or more complex cases.

Can You Go to Jail for Not Paying a Judgment?

In most cases, no, you cannot go to jail simply for failing to pay a civil judgment. Owing money is generally a civil matter, not a criminal offense.

However, a judgment shouldn’t be ignored. Courts may require you to appear for hearings, provide financial information, or comply with other collection-related orders. If you refuse to follow those orders, a judge could hold you in contempt of court. So if you’re unable to pay a judgment, it’s generally better to communicate with the court and the judgment creditor than to ignore the situation.

If you’re unable to pay a judgment, it’s generally better to communicate with the court and the judgment creditor rather than ignore the situation.

What Can a Creditor Do After Winning a Judgment?

Winning a judgment doesn’t automatically result in payment. If the judgment remains unpaid, the creditor can use legal action to recover the money owed. This can include wage garnishment, bank account levies, and liens placed on real estate or other property.

Once a judgment is given, creditors must follow court-approved procedures and comply with state and federal laws to collect the debt owed. Additional paperwork, notices, or court approvals may be required before collection efforts can proceed.

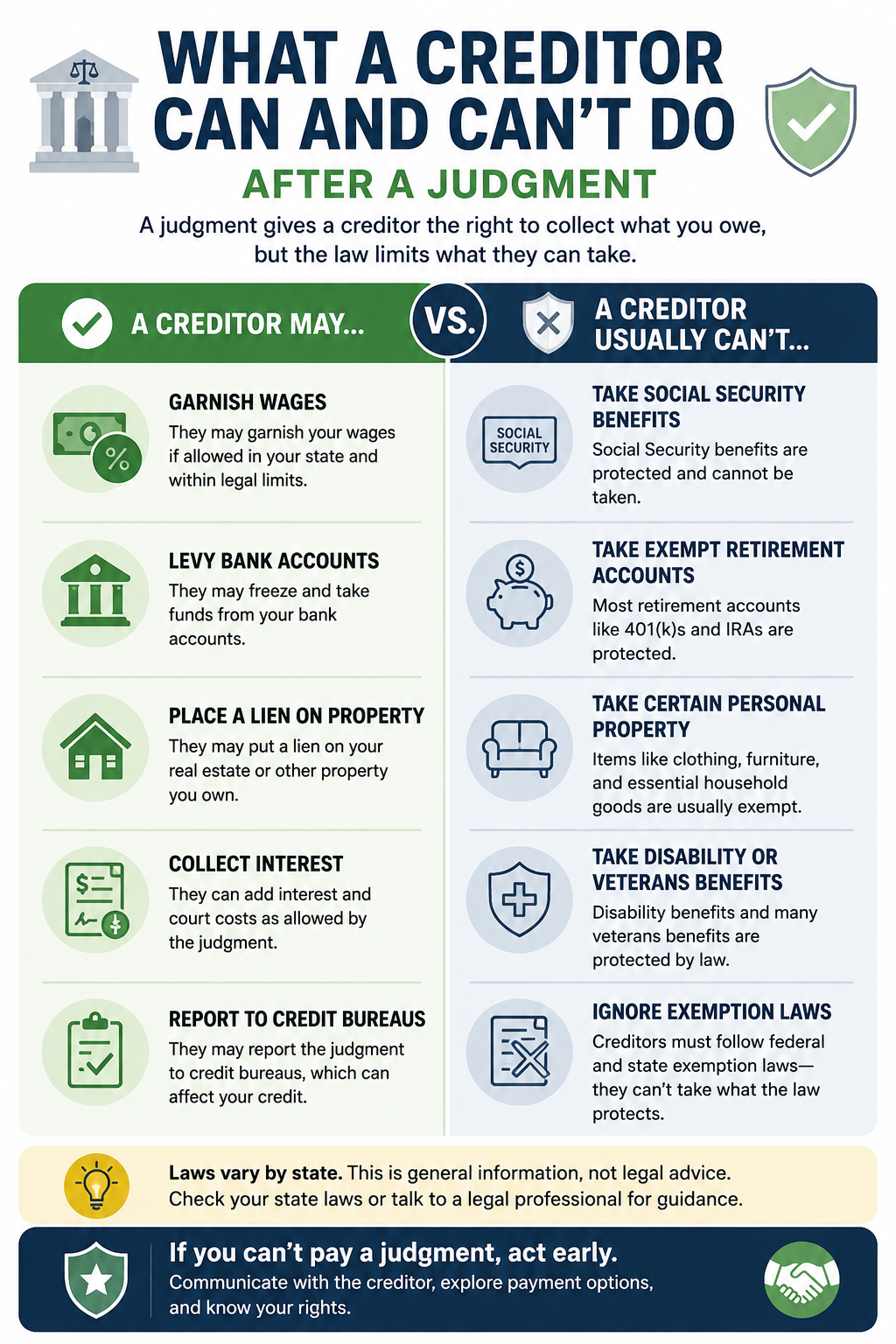

What a Creditor Can and Can’t Do After a Judgment

Not everything you own is automatically at risk after a judgment. This infographic compares the collection actions creditors may take with the income and property that are often protected by law.

What Is Protected From a Judgment?

A judgment doesn’t give the right to creditors to take funds from the debtor by any means necessary. Federal and state laws provide exemptions protecting certain types of property and income from creditors.

Common exemptions to judgments include:

- Home equity through a homestead exemption

- Certain personal property, such as clothing, furniture, and household goods

- Retirement accounts

- Essential household items and tools needed for work

Many states also protect income sources such as:

- Social Security benefits

- Disability benefits

- Veterans benefits

- Certain pension and retirement income programs

It’s also important to understand that an exemption doesn’t make the debt disappear. It simply limits what a creditor can take to satisfy the judgment. Even if some of your assets or income are protected, the judgment may remain valid until it’s resolved.

Can You Set Up a Payment Plan After a Judgment?

It’s still possible to negotiate a payment plan after a judgment. Many creditors would rather receive consistent payments than spend additional time and money pursuing collection efforts.

Depending on the circumstances and state law, courts may also approve or order structured payment arrangements. However, the availability of court-supervised payment plans varies by jurisdiction.

If you reach an agreement with the creditor, be sure to get the terms in writing and keep records of all payments. Sending important payment-related communications by certified mail with a return receipt requested can serve as evidence that someone received the document.

If you’re able to pay off the judgment, it generally should stop contact from the collector. If you can’t pay in full, communicating with the creditor may help you avoid more aggressive collection measures.

Can a Judgment Affect Your Credit or Future Borrowing?

A judgment can make it more difficult to qualify for a credit card, a car loan, or even a mortgage. Judgments are public records, and lenders can review public records or ask applicants about outstanding judgments during their underwriting process.

An active judgment may reduce your creditworthiness and make it harder to qualify for personal loans, debt consolidation loans, mortgages, business financing, or other forms of credit. Some lenders may require the judgment to be paid or resolved before approving an application. However, a judgment doesn’t automatically prevent you from borrowing, so be sure to check your entire credit history to see if you may qualify for financing options.

If you’re struggling with debt, be sure to consider options like debt consolidation or sitting with a nonprofit credit counseling agency to see if you can avoid the courts getting involved.

What Are Your Options If You Can’t Afford to Pay a Judgment?

If you can’t afford to pay a judgment, consider the following options:

Negotiate With the Creditor

In some cases, a creditor may be willing to work with you after a judgment is entered. You may be able to negotiate a lump-sum settlement for less than the full balance, or ask that collection efforts be paused while discussions are ongoing. Make sure all terms are documented in writing if you reach an agreement.

Set Up a Payment Plan

A payment plan with the creditor can spread payments over time. Be sure to keep detailed records of all payments and communications related to the agreement.

Ask About Hardship Programs

Some creditors offer hardship assistance for people experiencing financial difficulties. Programs may be available after job loss, illness, disability, or other qualifying hardships.

Work With a Credit Counseling Agency

A reputable nonprofit credit counseling agency can help you review your budget and debt obligations. Counselors may suggest repayment strategies or debt management plans that fit your financial situation. This strategy can be helpful if you’re struggling with multiple debts.

Consider Bankruptcy Carefully

Bankruptcy may be an option when a judgment debt is impossible to repay. However, bankruptcy carries significant long-term financial and legal consequences. It’s wise to consult a qualified bankruptcy attorney first.

Related Article: Debt Consolidation vs. Bankruptcy: Which Should I Choose?

Act as Early as Possible

Taking action early can help limit the consequences of an unpaid judgment. Judgments often accrue interest, which can increase the total amount owed over time. Contacting the creditor sooner rather than later may create more opportunities to negotiate a resolution.

Related Debt and Credit Resources

If you’re dealing with a judgment, you may also find these guides and calculators helpful. They cover debt consolidation, missed payments, budgeting, and other strategies for managing debt and improving your financial situation.

- What Is Debt Consolidation? Learn how debt consolidation works, who it’s best for, and when it may help simplify your finances.

- How to Choose the Right Debt Consolidation Plan: Compare your options and learn how to select the best strategy for your financial goals.

- Debt Consolidation for Bad Credit: Explore debt relief options if your credit score makes qualifying for a loan more challenging.

- What Happens If I Can’t Pay My Credit Card? Understand the consequences of missed credit card payments and the options available before debt escalates.

- What Happens If I Can’t Pay My Mortgage? Learn the mortgage delinquency timeline, foreclosure process, and ways to protect your home.

- What Happens If I Don’t Pay a Collections Agency? Find out what debt collectors can legally do and what rights you have during the collection process.

- How Late Can You Be on a Car Payment? Learn what happens after a missed car payment and when repossession becomes a possibility.

- Debt Snowball Calculator: See how quickly you could pay off debt using the popular debt snowball repayment strategy.

- Budget Calculator: Build a monthly budget to better manage expenses, reduce debt, and improve your financial health.

- Best Debt Consolidation Companies: Compare leading debt consolidation providers based on fees, customer experience, and overall value.

- Debt Consolidation Calculator: Estimate how much you could save by combining multiple debts into a single monthly payment.

What Happens After the Judgment Is Paid?

Once a judgment is paid in full, the creditor will typically file a Satisfaction of Judgment with the court. This document confirms that the debt has been paid and updates the court record to show that the judgment has been satisfied. In many states, creditors are required to file this paperwork within a certain timeframe after receiving payment.

After the judgment is satisfied, collection efforts related to that debt should stop. Wage garnishments, bank levies, and other enforcement actions are generally terminated, and any judgment liens may need to be formally released. It’s a good idea to keep copies of your proof of payment and any court filings in case questions arise later about the status of the judgment.