Missing a student loan payment can lead to late fees, credit reporting, and other consequences if the debt remains unpaid. Federal student loans typically enter default after 270 days of missed payments, which may result in wage garnishment or tax refund offsets. However, borrowers have options at every stage, including repayment assistance programs, deferment, forbearance, and default resolution programs.

If student loan payments are only part of your financial challenge, exploring professional debt solutions may help you better manage other unsecured debts at the same time. Learning more about Accredited Debt Relief can help you determine whether a debt solution could improve your overall financial situation while you explore student loan repayment options.

Here’s what you need to know if you’re unable to pay your student loans.

Key Takeaways

|

What Happens When You Miss a Student Loan Payment?

Missing a student loan payment doesn’t immediately put your loan into default. However, the loan becomes delinquent. During this period, your loan servicer will typically contact you to discuss repayment options.

Missed payments may be reported to the credit bureaus and could negatively affect your credit score. Your overall balance could increase if your lender applies late fees.

When Does a Student Loan Go Into Default?

Default generally starts after 270 days of missed payments on federal student loans. Private student loans are different, and default terms vary by lender.

If you reach default, the lender may demand immediate repayment of the full remaining balance rather than allowing you to continue making monthly payments. For federal loans, the Department of Education may transfer the debt to collections, and the negative impact on your credit report can become much more severe.

What Can the Government Do If You Default on Federal Loans?

Federal student loans come with collection powers that private lenders don’t have. The government may use the Treasury Offset Program to take some or all of your federal tax refund and apply it toward your debt.

The government may also garnish a portion of your wages without first obtaining a court order. In some cases, a portion of Social Security benefits can also be withheld to repay defaulted federal student loans. These enforcement tools are generally limited to federal student loans and are not available to private lenders.

What Can Private Lenders Do If You Default?

Private lenders have fewer collection powers than the federal government, but default can still have serious consequences. A lender may send the account to a debt collection agency and report the default to the credit bureaus, which can significantly damage your credit score. Private lenders generally must obtain a court judgment before they can garnish wages or pursue certain collection actions.

Private student loans offer fewer repayment protections, hardship programs, and forgiveness options than federal loans. If you’re struggling with private student loan payments, refinancing your student loans may be an option worth considering.

How Does Student Loan Default Affect Your Credit Score?

Missing student loan payments can hurt your credit long before a loan reaches default. Delinquent payments may be reported to the credit bureaus and can lower your credit score, especially if payments are 30 days or more past due.

Default causes more significant damage because it signals a serious failure to repay the debt. If the account is sent to collections, additional negative information may appear on your credit reports. In most cases, delinquent payments and default-related marks can remain on your credit reports for up to seven years. A damaged credit history can make it harder to qualify for credit cards, auto loans, mortgages, and other forms of borrowing in the future.

What Options Do You Have Before You Default?

If you’re struggling to make payments, it’s important to contact your loan servicer as soon as possible. The earlier you act, the more options you’ll typically have to avoid default.

Federal borrowers may also be eligible for an income-driven repayment (IDR) plan, which sets monthly payments based on your income and family size rather than the amount you owe. You may qualify for deferment or forbearance, which can temporarily pause your monthly payments.

If you have private student loans, refinancing may help reduce your interest rate or monthly payment. However, refinancing federal loans into a private loan generally causes you to lose access to federal benefits.

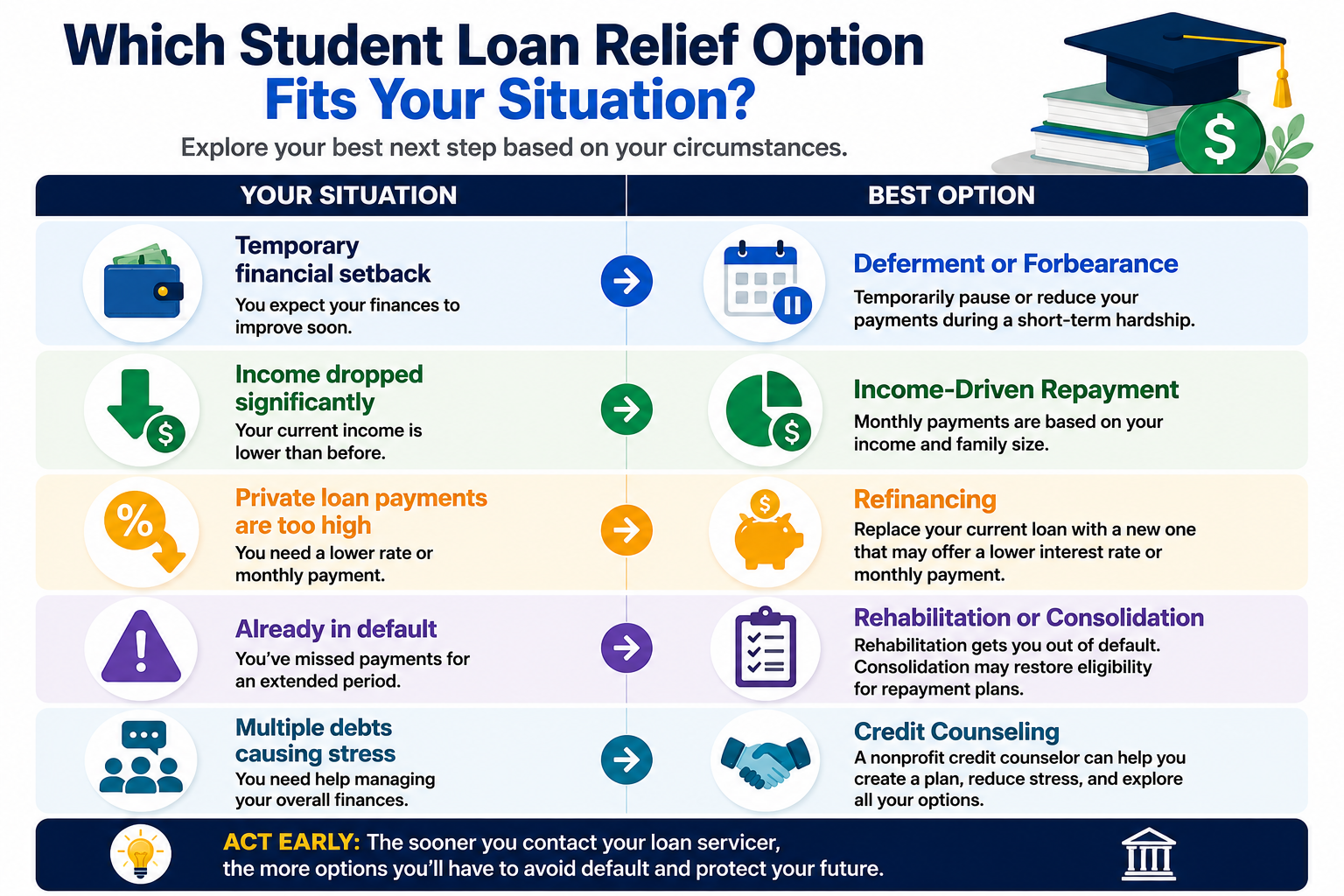

Not all student loan problems require the same solution. This infographic matches common financial situations with student loan relief options that may help borrowers avoid default and regain control of their finances.

What Options Do You Have After You Default?

Default doesn’t mean you have run out of options. For federal student loans, loan rehabilitation allows borrowers to remove a loan from default by making a series of agreed-upon monthly payments. Another option is federal loan consolidation, which can move a defaulted loan into a new Direct Consolidation Loan and restore eligibility for certain repayment programs.

For private student loans, options may include negotiating directly with the lender, requesting hardship assistance, considering debt consolidation, or working out a modified payment arrangement. A nonprofit credit counseling agency may also help you evaluate your finances and repayment options.

In severe situations, bankruptcy may be worth discussing with an attorney. Although discharging student loans in bankruptcy can be difficult, it’s possible in some circumstances.

Can Student Loan Debt Affect Other Parts of Your Financial Life?

Student loan debt can make it harder to qualify for a home loan, a car loan, a new credit card, and even impact your ability to get a job. Lenders often review your debt-to-income (DTI) ratio, which compares your monthly debt payments to your income. Higher student loan payments can increase your DTI ratio and reduce your borrowing power.

Addressing student loan debt through repayment programs, rehabilitation, refinancing, or debt consolidation strategies may help improve your overall financial stability and make it easier to reach other financial goals.

Related: What Happens If I Can’t Pay My Mortgage?

Further Reading

- Debt Consolidation with Bad Credit: What to Expect and How to Qualify

- Alternatives to Bankruptcy: Try This Option First

- Credit Card Debt Is Soaring. Here’s How You Can Escape It

- Millions of Car Owners Face Late Car Payment Difficulties

- How Late Can You Be on a Car Payment Before You Lose Your Car?

- Credit Card Debt Forgiveness: What’s Real and What’s a Scam

- Best Debt Consolidation Companies of the Year

- What Happens If I Can’t Pay a Judgment?