The Short Answer: How Much Money Should I Save Before Buying a House?

Saving money for a home is mostly about your down payment, but it also includes closing costs and a financial cushion after you move in. Equifax (a major credit bureau) has recommended saving 25% to 35% of the home’s purchase price, which typically covers:

- Down payment

- Closing costs

- Upfront moving and setup costs

- Early repair and maintenance buffer

A common rule of thumb is to aim for 20% down if possible, but the “right” number depends on your budget, credit profile, and loan type.

Key Takeaways

|

Why There Is No One-Size-Fits-All Savings Number

That 25% to 35% range is broad because buyers’ finances and home prices vary widely. While a 20% down payment might be realistic in one market, it could be nearly impossible in another.

Key variables that change your target:

- Local home prices and your income

- Closing costs (often 3% to 5% of purchase price)

- Extra fees (attorney, repairs, inspections, moving)

- Loan programs (FHA and other low-down options)

- Credit strength (which can affect approval, pricing, and required cash)

A bigger down payment can reduce monthly costs and interest over time, but over-stretching can backfire if it wipes out your emergency fund. The best plan balances down payment + closing costs + stability.

Related Article: Should I Buy a Car or House First?

Key Costs to Save for Before Buying a Home

1. Down Payment Savings and the Home’s Purchase Price

A higher down payment usually means:

- Lower monthly payment

- Less interest over the life of the loan

- Less need for add-ons like PMI (depending on the loan)

Some lenders also allow mortgage discount points (often 1% of the loan amount per point) to reduce your interest rate. This can lower long-term costs, but only makes sense if you plan to keep the loan long enough to benefit.

2. Closing Costs and Upfront Fees When Buying a Home

Many buyers plan for the down payment and then get surprised by closing costs. Closing costs may include:

- Loan origination and processing fees

- Appraisal and underwriting costs

- Title services and insurance

- Attorney fees (in some states)

- Prepaid items like property taxes and homeowners’ insurance (varies)

Even when seller credits or negotiations are possible, buyers should not assume closing costs will be fully covered.

3. Emergency Fund and Extra Cash for New Homeowners

Owning a home often comes with costs renters never see. Even with an inspection, issues can show up after closing. A practical post-purchase cushion can help cover:

- Repairs and maintenance

- Utility deposits or higher utility bills

- Initial purchases (tools, lawn care, minor upgrades)

- Unexpected changes (job loss, medical expenses)

A strong down payment is helpful, but a drained bank account can make homeownership stressful fast.

Pro Tip: Quick Planning ReminderFrom our on-staff Certified Financial Educator Keep these in mind when planning your home purchase:

|

How Your Debt, Credit Cards, and Credit Score Impact How Much You Need to Save

Even with savings, your monthly debt payments matter because they reduce your flexibility once a mortgage payment is added. If debt payments already feel tight, you may need more cash reserves to stay stable.

Debt-to-Income Ratio and Mortgage Approval

Lenders look closely at the debt-to-income (DTI) ratio, which compares your monthly debt payments to your income.

A higher DTI can:

- Limit how much you can borrow

- Push you into less favorable loan terms

- Increase the amount of savings you need for safety

Saving While Carrying Credit Card, Auto, or Personal Loan Debt

There’s a balancing act between saving and paying down debt.

General guideline:

- High-interest debt (often credit cards, many personal loans): paying it down can be more impactful than saving extra, because the interest cost is usually higher than savings yields.

- Lower-interest debt (often auto loans): still affects cash flow, but the urgency may be different.

When Debt Consolidation Can Improve Your Home-Buying Readiness

Taking out a new loan right before applying for a mortgage can complicate approval. But when done early enough, debt consolidation may help by:

- Reducing total monthly payments

- Simplifying multiple balances into one payment

- Helping you pay down debt faster

If consolidation is part of your plan, do it well ahead of your mortgage timeline so you can show a consistent repayment history.

How Interest Rates, PMI, and Loan Types Affect How Much You Should Save

1. How Interest Rate Changes Affect Monthly Mortgage Payments

Rates don’t have to move much to change affordability. Even a small rate increase can raise your payment enough to strain your monthly budget. Also consider the loan structure:

- Fixed-rate mortgages offer predictable payments.

- Adjustable-rate mortgages can change over time, increasing payment risk.

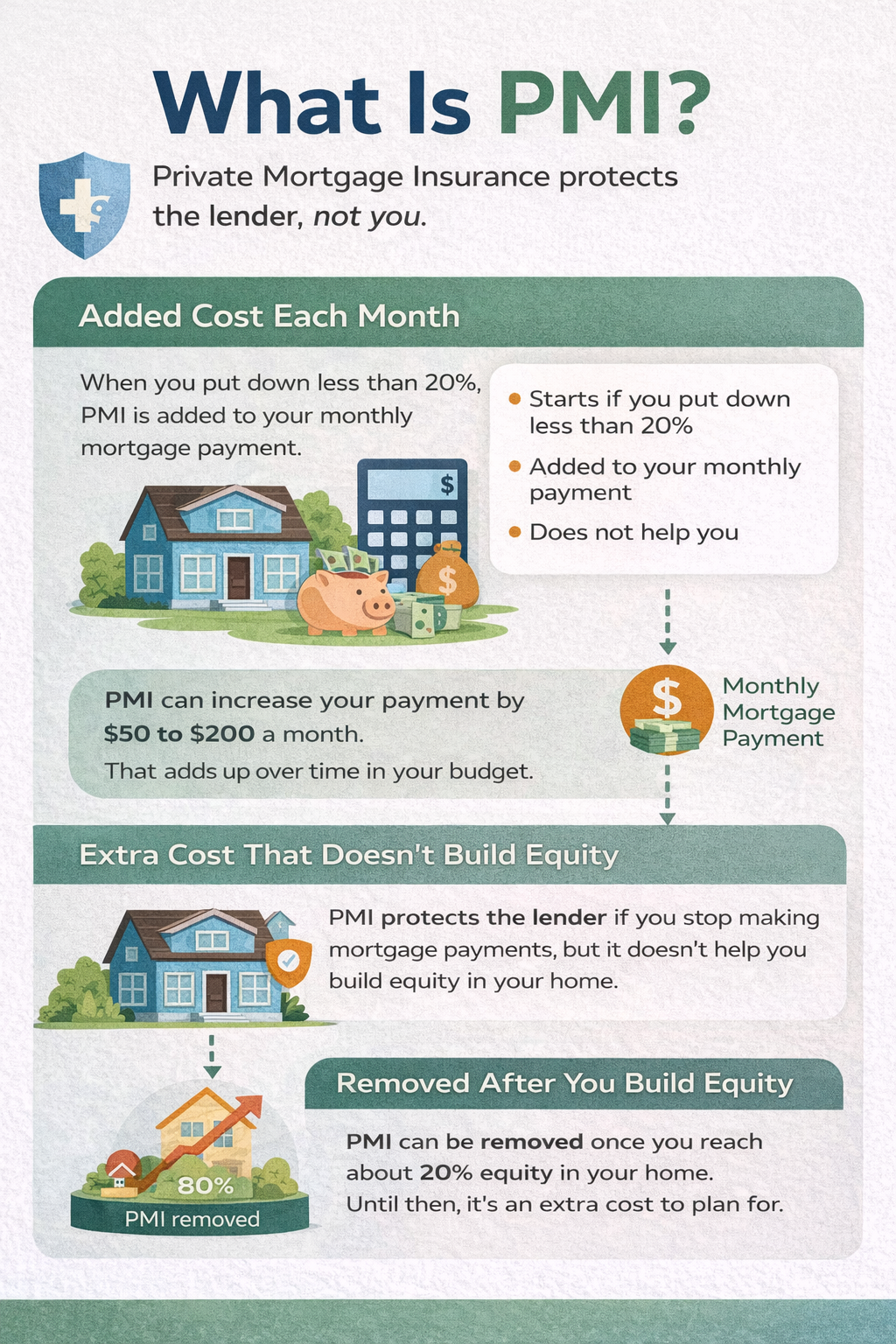

2. Private Mortgage Insurance and How It Affects Your Budget

PMI is often required when the down payment is below a certain threshold. It may not look huge on paper, but it can be enough to change what “affordable” means in your monthly budget.

What is PMI? A simple breakdown of private mortgage insurance and how it impacts your monthly budget when buying a home.

3. FHA Loans and Other Loan Programs for First-Time Home Buyers

Programs like FHA can lower down payment requirements, but they may come with restrictions tied to:

- Property type and condition

- Purchase price limits (by region)

- Program availability and qualification rules

They can be helpful, but it’s important to understand the tradeoffs before choosing a low-down option. Check out our overview of the Best Mortgage Lenders for even more information.

How to Manage Your Budget While Saving for a House

1. Understanding Your Monthly Cash Flow

Before deciding how much to save, get clear on your monthly cash flow:

- Fixed expenses: rent, insurance, subscriptions, minimum debt payments

- Variable expenses: groceries, fuel, utilities, dining out, household spending

This, and more tips from the Consumer Financial Protection Bureau, can help you estimate how much room you really have for a future mortgage payment.

Related Article: Does Debt Consolidation Affect Buying a House?

2. Balancing Saving for a House and Paying Down Debt

A practical approach:

- List debts by interest rate and monthly payment

- Prioritize the balances that cost you the most in interest

- If payments feel unmanageable, explore consolidation tools early

3. Adjusting Your Budget Without Sacrificing Financial Stability

Cutting everything can backfire if you end up relying on credit cards or skipping essentials. Aim for sustainable changes that still protect stability, especially while interest keeps accruing on existing debt.

How Much to Save If You’re Buying a House on a Tight Budget

1. Minimum Savings vs. Ideal Savings

A 20% down payment is often ideal, but it’s not always required or best. If you’re tight on savings, prioritize:

- Down payment that fits your loan type

- Closing costs buffer

- Emergency fund for early homeowner surprises

2. Signs Your Financial Situation May Need More Time

Delaying a purchase can be a smart move if:

- Your job or income feels unstable

- Debt payments already stretch your budget

- You don’t have any emergency cushion

- A mortgage would make you “house poor” (high housing costs relative to income)